Weekly Market Outlook 03/08/2026

Conflict intensifies

Hello traders,

I hope you all had a great weekend.

The Iran-USA war has intensified over the weekend and the developing story is that USA has started to bomb refineries in Iran. What does this mean for the region and the world.

The first scenario is that Tel Aviv may have received indications that the U.S.-backed military campaign could reach a conclusion within approximately one week. Should this be the case, Israel may be acting with urgency to neutralize assets critical to Iran’s primary revenue streams before that window closes.

The second scenario involves a deliberate effort to provoke an Iranian response by directing strikes at oil infrastructure within the Gulf states, thereby extending the duration of the conflict. Such an escalation could significantly heighten tensions, potentially prompting the Islamic Revolutionary Guard Corps to abandon restraint and adopt a substantially more aggressive posture.

At present, the region appears to be entering an increasingly volatile phase. Wishing safety and well-being to the innocent across the Gulf.

We were short equities and long crude oil and closed our USO 80/95 spreads as they entered max gain last week.

We are still holding our /ES short and would like to hold it until 6844 or so (stops in +40 pt profit)

Realtime Discord access with equity positions tracker(new website rolling out to select subscribers), intraday orderflow & option dealer summaries included with the paid newsletter membership . Click here to subscribe.

Moving on,

Labor Market Weakness Versus Persistent Wholesale Inflation

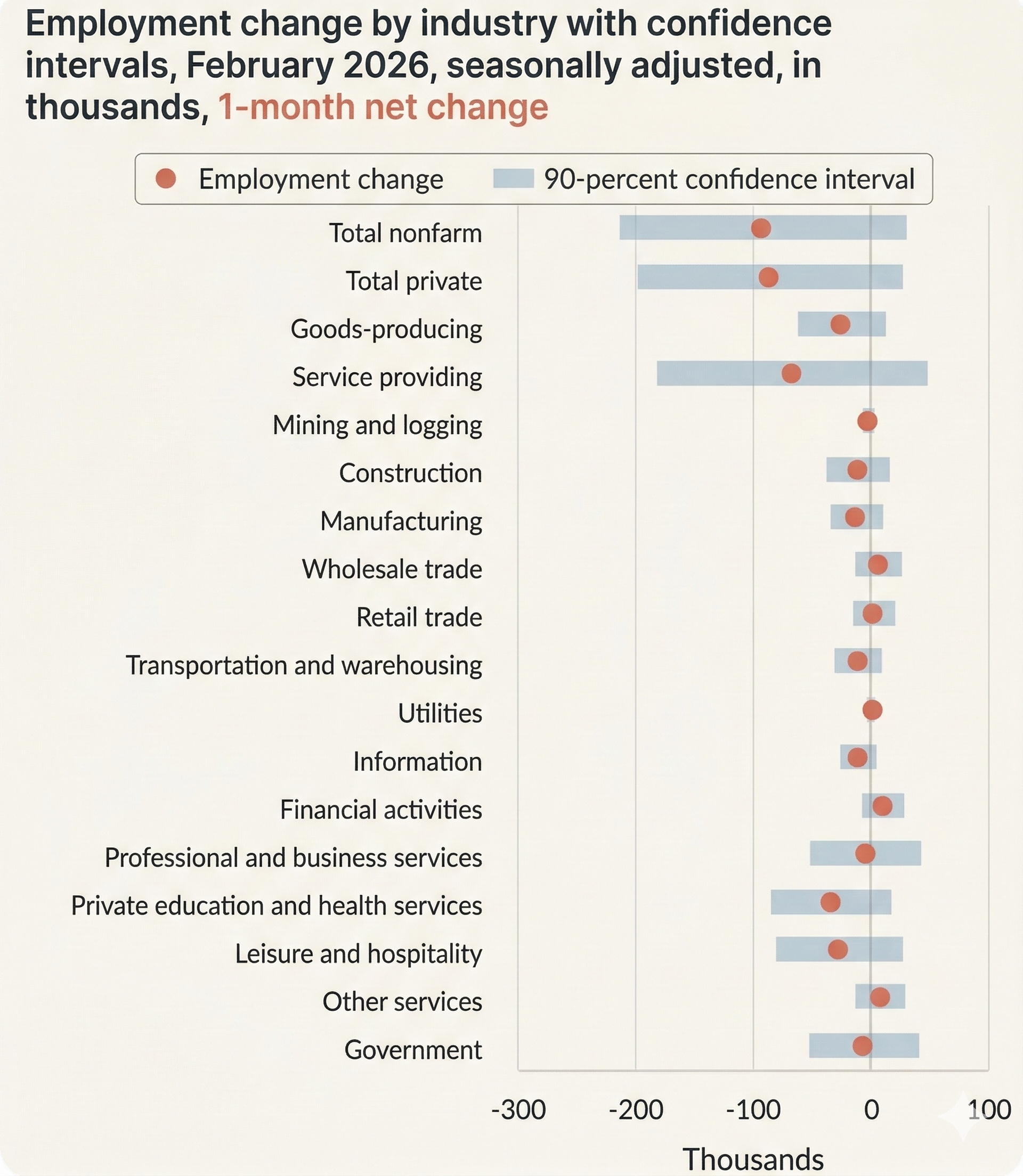

The economic data released in early 2026 paints a difficult and unusual picture. On one hand, the labor market appears to be weakening fast. The preliminary February employment report showed nonfarm payrolls falling by 92,000, with the unemployment rate rising to 4.4 percent. That is a sharp reversal from the stronger job growth seen in January and suggests that tight credit conditions, along with higher input costs tied to global supply chain strain, are starting to force companies to cut staff more broadly. The weakness was not limited to one corner of the economy. Financial services posted their worst hiring month since April 2025, while overall job growth leaned heavily on steadier sectors such as healthcare and education.

At the same time, inflation has not eased in the way higher interest rates were supposed to encourage. Headline CPI for January cooled modestly to 2.4 percent year over year, but wholesale inflation remained stubbornly strong. The final demand Producer Price Index rose 0.5 percent month over month, above expectations for 0.3 percent. Core PPI, which excludes food and energy, jumped 0.8 percent in a single month. With core PPI running at 3.6 percent year over year, price pressures are still building in the production pipeline, raising the risk that those costs will eventually flow through to consumers.

The Federal Reserve’s Dual Mandate Problem

That mix of softer employment and persistent inflation has thrown markets into confusion over what the Federal Reserve will do next. Before the February jobs report, the CME FedWatch Tool showed a 94.1 percent chance that the Fed would leave rates unchanged at its March meeting, largely because earlier labor data had looked solid. The payroll decline changed that view quickly. Traders in fed funds futures and interest rate swaps sharply repriced expectations, and the FedWatch Tool now points to a 97 percent chance that the Fed will cut rates to a range of 3.50 percent to 3.75 percent at the March 18 meeting.

At the same time, there are signs of a deeper split inside the Fed itself. More dovish policymakers, focused on the labor market’s sustained softness over the past six months, are said to support as many as four additional 25 basis point cuts this year to avoid a hard landing. More hawkish officials remain focused on the fact that core inflation is still well above the Fed’s 2.0 percent target. Their concern is that cutting rates too quickly, especially during a large oil price shock driven by geopolitical tensions, could push long-term inflation expectations higher and revive mistakes associated with the 1970s. Because Fed officials are now in the blackout period before the next FOMC meeting, investors will not hear any public guidance from Chair Jerome Powell, Governor Christopher Waller, or Vice Chair Michelle Bowman during the week of March 8 to 14. For now, markets are left to react almost entirely to incoming data.

So Algo, how does this impact the markets?