Weekly Market Outlook 2026/07/05

Storm before the calm

Hello traders,

Hope everyone had a great long weekend and enjoyed your 4th of July celebrations.

We had an excellent week last week where we caught the market drop midweek.

Other than that our AI next inning stock picks are off to a great start with a couple picks going up 1500-3000bps on the week.

Realtime Discord access with equity positions tracker(new website rolling out to select subscribers), intraday orderflow & option dealer summaries included with the paid newsletter membership . Click here to subscribe.

Last week’s market

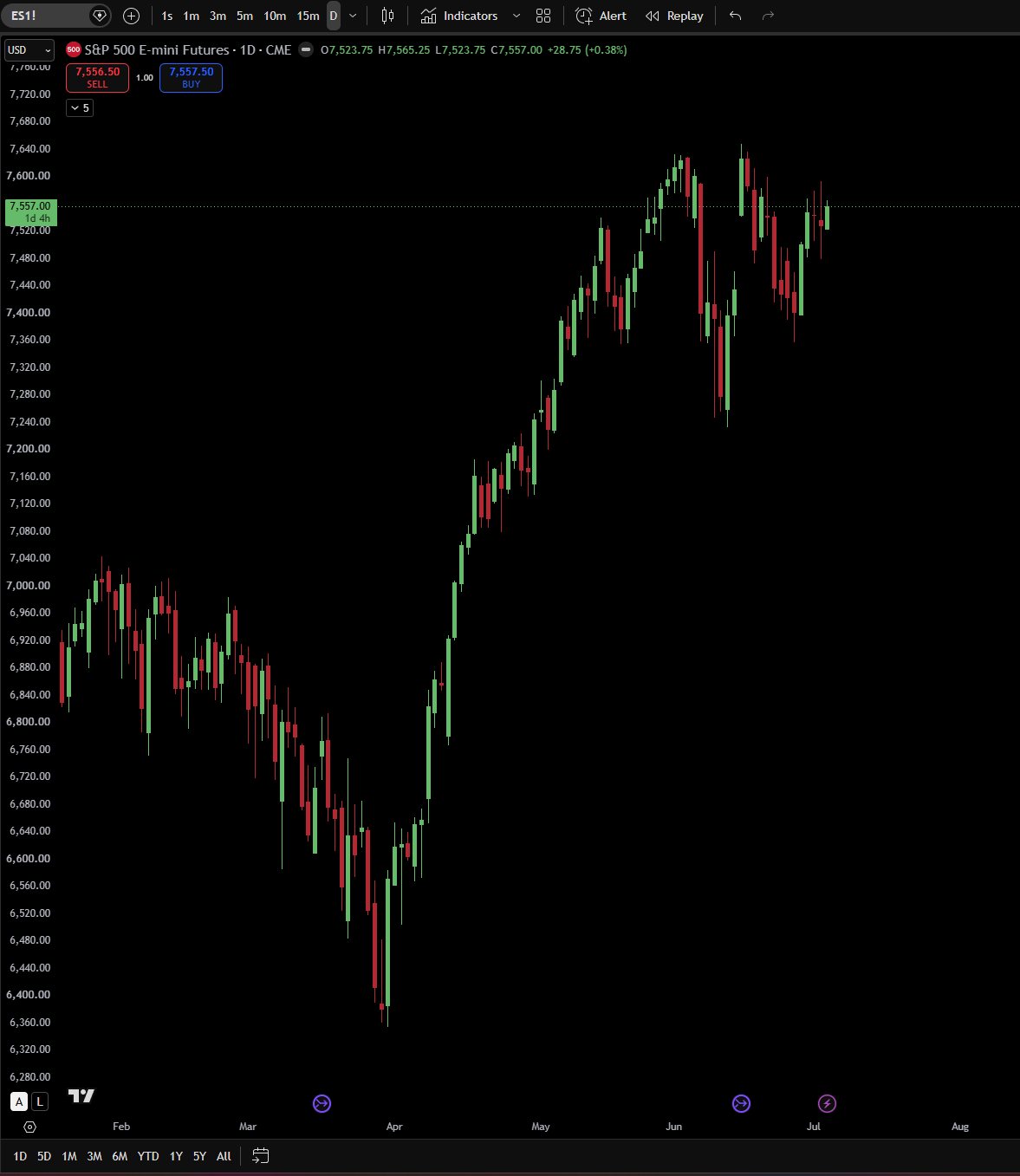

E-mini S&P 500 futures ended the week near 7,557. They gained about 210 basis points.

The Dow gained nearly 200 basis points and closed at 52,900.07 on July 2. The Nasdaq 100 ended near 29,900 after falling about 182 basis points in the final session. The Russell 2000 lost roughly 75 basis points for the week.

Semiconductors accounted for much of the Nasdaq’s weakness. The PHLX Semiconductor Index had risen more than 80% during the first half of 2026. The VanEck Semiconductor ETF then fell about 11% to 12% over two days in early July.

Reports said SK Hynix may slow its expansion of high-bandwidth memory production. That added to concerns that companies may be spending too much on AI infrastructure.

The semiconductor selloff did not spread across the whole market. The advance-decline line reached a new high. About 63% of stocks were above their 20-day moving averages, and 60% were above their 50-day moving averages.

These figures do not suggest broad weakness. They show that money has moved out of some technology shares and into other parts of the market.

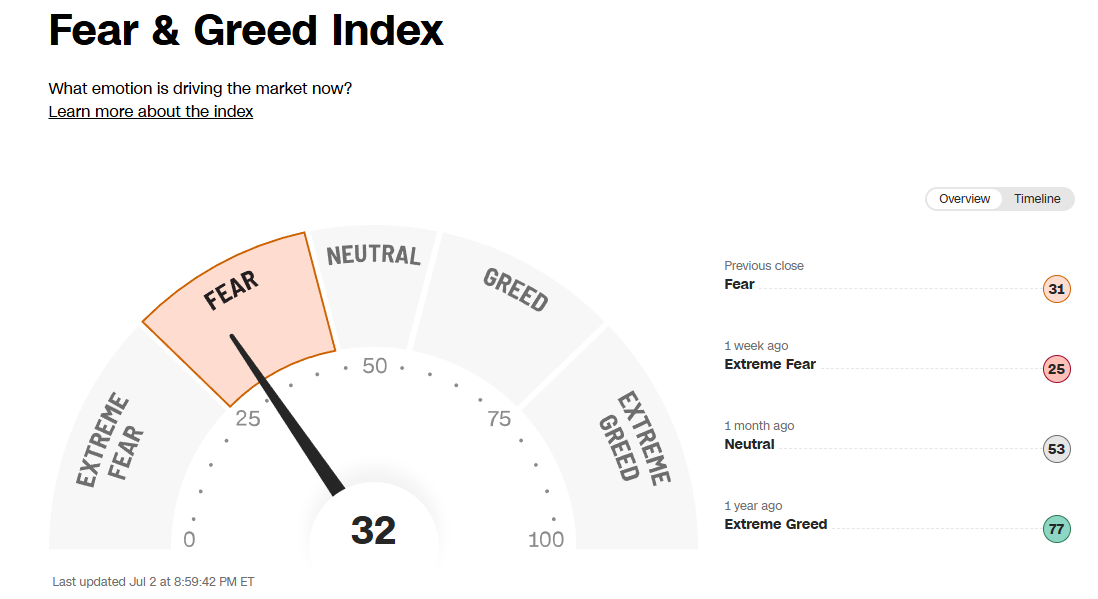

CNN’s Fear and Greed Index remains in “Fear” territory. It recently moved up from “Extreme Fear.” This is a cautious reading for a market trading near record highs.

Institutional exposure to cyclical stocks is in the eighth percentile. If those stocks continue to rise, some managers may have to increase their holdings. Private equity was the best-performing factor last week. Momentum was the worst.

The Magnificent Seven are down about 130 basis points this year. Investors have sold these shares to fund purchases elsewhere. They have also questioned whether the companies will earn enough from their large capital-spending programs.

The companies say they are spending because they do not have enough capacity to meet demand. Their stocks have recently formed a higher low and remain above the trend that began after the Liberation Day lows in 2025.

June employment report

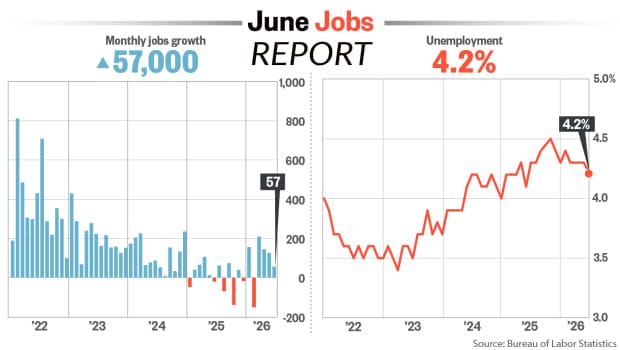

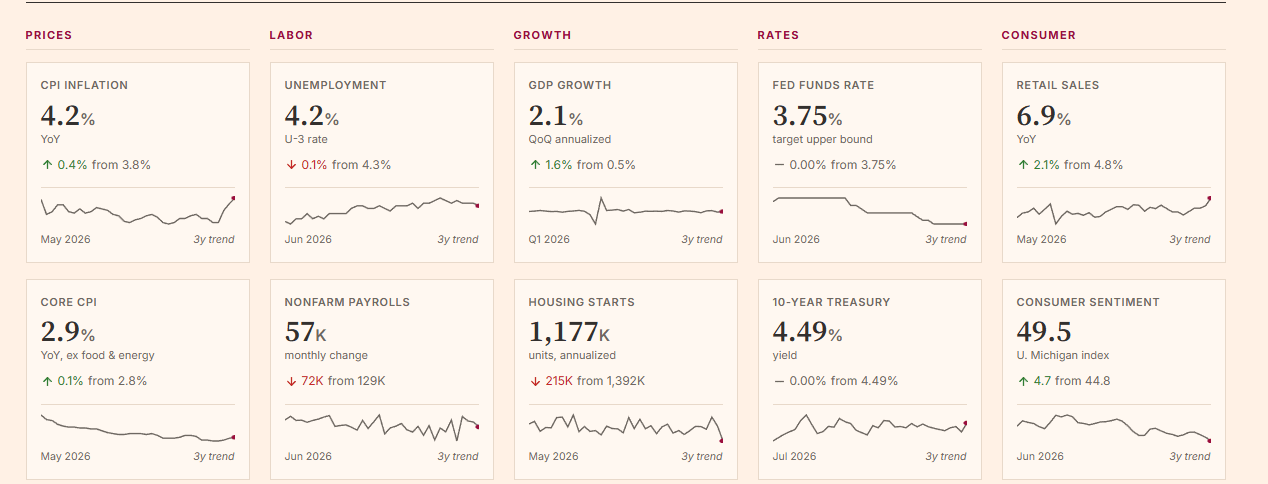

The economy added 57,000 nonfarm jobs in June. This was well below the consensus estimate.

The previous two months were revised lower. April was cut from 179,000 jobs to 148,000. May was cut from 172,000 to 129,000. The two revisions removed 74,000 jobs from the earlier estimates.

The unemployment rate fell from 4.3% to 4.2%. This was not the result of stronger hiring. Labor-force participation fell by 0.3 percentage points to 61.5%, its lowest level since March 2021.

Hospitality employment fell by 61,000. That was surprising because the World Cup should be increasing demand for travel, hotels, and restaurants in the United States.

The report points to a slower labor market. It does not yet point to a recession.

Higher-income households are still spending. Housing remains weak, and lower-to-middle-income households are under more pressure. The Fed will have to consider that weakness before raising rates again.

Federal Reserve

Warsh’s first meeting as Fed chair took place on June 16 and 17. The committee voted 12-0 to keep the federal funds rate between 3.50% and 3.75%.

The new economic projections were more hawkish than expected. The median forecast for core PCE inflation in 2026 rose from 2.7% to 3.3%. The median year-end interest-rate forecast increased to 3.8%. That forecast includes at least one rate increase before December.

Warsh shortened the FOMC statement and removed much of its forward guidance. At his press conference, he said, “This Committee will deliver price stability.” He also said inflation required “immediate triage.”

His comments since the meeting have been less hawkish. He acknowledged that inflation conditions have improved as oil prices have fallen. This appears to rule out a July increase.

At the ECB Forum in Sintra, Warsh said inflation was still too high. He did not give a timetable for future rate changes.

Markets put the probability of at least one increase this year at about 65%. Current pricing is close to an 80% chance of an increase and a 20% chance of no change.

My estimate is closer to a 40% chance of an increase and a 60% chance of no change.

Conditions are different from those in 2022. Fiscal policy is less expansionary. Supply chains are working better. Housing is weak, and some consumers are under pressure. Oil has also fallen from its recent high.

Net immigration has turned negative, which may limit the supply of workers. AI could improve productivity and reduce some costs over time. It is too early to know how large that effect will be.

Warsh has said AI should reduce inflation over the long term. He has also said that strong economic growth and employment do not always cause higher inflation. Those views give him a reason to leave rates unchanged if the data remain mixed.

Crude oil is back near its pre-war price in the mid-$60s. The 10-year Treasury yield remains above its pre-war level. Lower energy prices may eventually pull yields down as well.

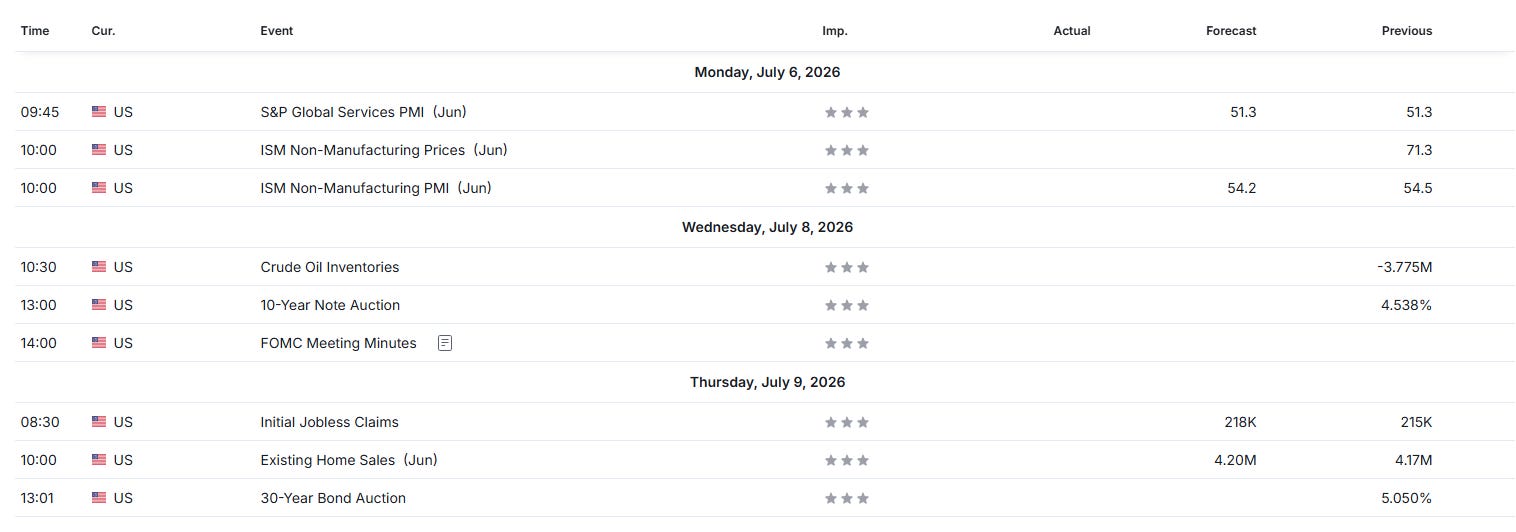

The June FOMC minutes will be released Wednesday at 2:00 p.m. ET. The minutes may show whether committee members agree with Warsh’s public position. They may also show how officials view inflation, employment, and the effect of AI on productivity.

Treasury market

The 10-year Treasury yield ended the week in the mid-4.40% range. It recently found support near 4.35%.

Bond prices have remained weak even though crude oil has fallen. The Fed’s June projections are one reason. The upcoming Treasury supply may be another.

Warsh’s focus on inflation may help long-term bonds. Investors are less likely to demand a large inflation premium if they believe the Fed will keep inflation under control.

Three auctions are scheduled this week 3y, 10y, 30y

The June 10 auction of 10-year notes cleared at 4.538%. The secondary-market yield was 4.49% on July 2.

The bid-to-cover ratio will show how much demand each auction receives. Indirect bidding will give some indication of demand from foreign institutions and central banks.

Weak demand would probably push yields higher. Strong demand would support bond prices.

I think Treasury prices have more room to rise than fall at current levels. If oil stays down and economic growth continues to slow, the 10-year yield could move toward 4.20%.

A range between 4.35% and 4.50% is still possible until inflation data improve. A move above 4.60% would weaken the bullish case for bonds.

U.S. dollar

The Dollar Index lost some of its post-FOMC gains last week. It has returned to its 20-day moving average.

The dollar has been in a longer-term decline since Trump’s inauguration in 2025. The recent rally has not yet changed that trend.

The level at 97.9 is important. A break below it could lead to a move toward the 200-month moving average near 93.

If 97.9 holds, the index may continue trading between that level and 103. The upper end of that range is close to where the dollar traded before Liberation Day.

The dollar’s recent strength came from expectations of higher U.S. rates. If those expectations fall, the dollar should lose support.

Crude oil

West Texas Intermediate crude ended the week near $68.78. It is down more than 40% from its 2026 high.

The June 17 Islamabad Memorandum of Understanding between the United States and Iran opened a 60-day period for negotiations. Oil tanker traffic through the Strait of Hormuz also resumed. These developments reduced fears of a major supply interruption.

OPEC+ is adding supply. On July 5, seven members announced that they would increase production by 188,000 barrels per day starting in August.

The group could pause or reverse the increase later. For now, the change adds more oil to the market.

The ISM Manufacturing Prices component fell from 82.1 to 73.0 in June. The 9.1-point decline was the largest since July 2022. The index is still high, but input-price pressure has eased.

WTI may trade between the mid-$60s and low-$70s if the situation in the Middle East does not get worse.

A break below the mid-$60s would probably require weaker demand from China or a larger increase in OPEC+ production.

Iran and Israel

Iranian naval activity has increased again. The threat rating for the Strait of Hormuz is now “substantial.”

Iran and Israel have continued to exchange strikes despite the ceasefire arrangements. Israel is also still carrying out operations in southern Lebanon. Those operations continued after the June 19 ceasefire between Israel and Hezbollah.

Hardline groups in Iran oppose the talks with the United States. They are also demanding that the United States reduce its presence in the region.

The United States has criticized some Israeli operations in Lebanon. U.S. officials are concerned that the fighting could hurt negotiations with Iran.

The talks have a 60-day window. If they continue, some of the remaining war premium should come out of oil. If they fail, oil prices could rise quickly.

Higher oil prices would add to inflation and make the Fed more likely to raise rates.

Trade policy

Relations between the United States and China are quiet for now.

Both countries are discussing lower tariffs on agricultural products. China has also agreed to buy large amounts of U.S. soybeans through 2028.

The United States declined to renew USMCA on July 1. The agreement will now go through annual reviews that may continue until 2036.

A new trade agreement with the European Union took effect on July 1. It applies a 15% tariff to most European products.

The 10% global surcharge under Section 122 is scheduled to expire on July 24. The United States has proposed Section 301 tariffs for several countries as a possible replacement.

The USMCA decision creates some uncertainty for North American businesses. The agreement is not about to expire, so the immediate effect should be limited.

ECONOMIC CALENDAR

Wednesday has the most event risk. The 10-year auction starts at 1:00 p.m. The FOMC minutes follow one hour later.

Weak auction demand and hawkish minutes would probably push yields higher. Strong demand and less hawkish minutes would probably lower them.

The ISM Services report is due Monday. Its price components will show whether inflation in the service sector is easing.

June CPI will be released July 14. PPI follows July 15. Those reports will be more important than this week’s data for the inflation outlook.

Market Biases

ES Emini

Bias: