Weekly Market Outlook 3/30/2025

What a year captain, it's only March

Hello traders,

We had an interesting week in the markets with the indices closing at the lows on Friday and dropped further into settlement.

But first, a recap of last week’s select trades.

Textbook EOD long on Monday on ES.

Similar idea, slightly weird execution.

Wednesday, we had a lacklustre day on futures but were able to recover through QQQ options.

Perfect range-day on Thursday

Mother of All Trend days on Friday

Moving on,

US consumer confidence on Friday created peak recession fears in the market.

The University of Michigan's conclusive sentiment index for March exhibited a notable decrement, descending to 57 from the preceding month's figure of 64.7. This most recent assessment fell short of both the preliminary estimate of 57.9 and the median projection derived from a Bloomberg survey of economic experts.

According to the data disseminated on Friday, consumers anticipate a sustained inflationary trajectory, with prices projected to escalate at an annualized rate of 4.1% over the forthcoming five to ten-year period. This prognosis represents the most elevated expectation since February 1993, surpassing the initial reading of 3.9%. Furthermore, respondents foresaw a 5% surge in costs over the ensuing twelve months, marking the highest short-term inflationary outlook since 2022.

Trump said he couldn’t care less if the tariffs made cars expensive.

I’m not an economist but this definitely looks like the administration genuinely does not care about the stock market or the economy in the short term.

Moreover, the AAII Investor sentiment has flipped extremely bearish.

Now, with all the doom and gloom, should we all just flip short?

Not so fast, bucko.

We are not even at the median annual drawdown on SPX since its inception.

Sex and Fear are the two things that sell exceptionally well.

But historically it has been proven time and again that being invested in the indices is better than flipping to cash/bonds for majority of investors.

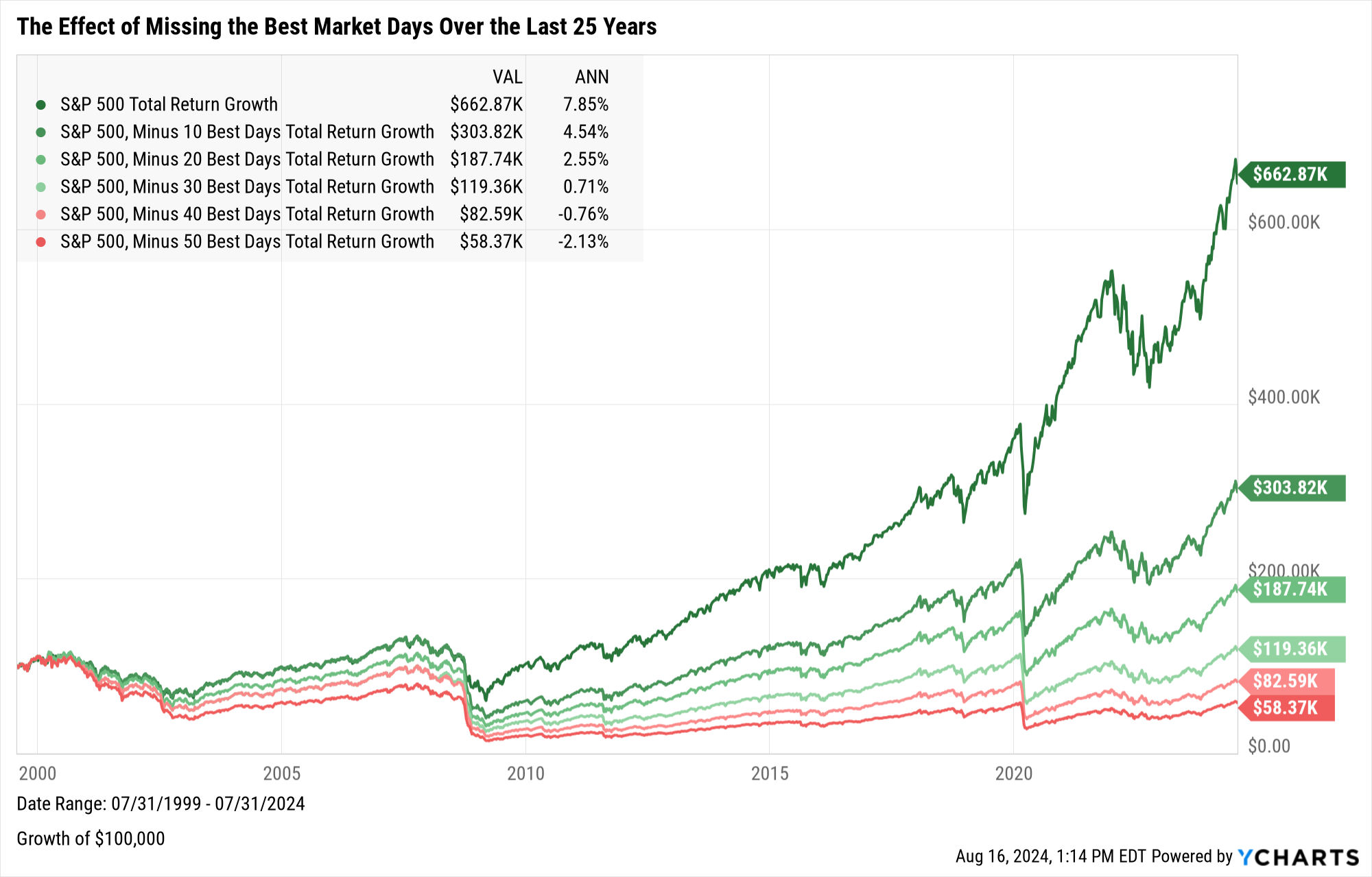

Over the past quarter-century, the S&P 500 has proven a formidable engine of wealth creation, elevating a $100,000 investment to $662,870 by July 31, 2024, a reflection of a steady 7.85% annualized return. Yet, the risks of attempting to time the market emerge sharply when one examines the cost of missing its strongest days.

Excluding just the 10 best-performing days slashes the portfolio’s value to $303,820, cutting the annualized return to 4.54%. The toll mounts with each additional absence: missing the top 20 days yields $187,740 at 2.55%, while skipping the top 30 days dwindles the sum to $119,360, with a mere 0.71% return. The decline turns punitive beyond that—omitting the top 40 days reduces the investment to $82,590, a negative 0.76% annualized return, and missing the top 50 days leaves just $58,370, a dismal -2.13% return.

A visual depiction of these scenarios reveals a striking contrast. The S&P 500’s unbroken path demonstrates resilience through turbulent periods, including the early 2000s downturn and the 2008 financial crisis. In contrast, each instance of missed days traces a flatter, diverging arc, underscoring the steep price of being sidelined during pivotal market surges.

The lesson is unmistakable: enduring the market’s ups and downs, rather than dodging them, remains essential to capturing its full potential for long-term gains.

If you zoom out even further, the noise in-between looks laughable.

Okay, I get off my soap-box now (finally!)

This week presents a plethora of economic data unveilings, with the April 2 tariff deadline and the April 4 Non-Farm Payrolls report emerging as the linchpins of critical significance.

Should the SPX manage to revisit and spring upward from its March lows of 5507, advocates of an optimistic market outlook would breathe a collective sigh of relief. Failing that, a rendezvous with the 5302 level looms on the horizon.

Nonetheless, this should be an interesting week and I would provide more updates through X and Telegram through the week.

Weekly Levels:

Subscribers are urged to use the tradingview indicator to plot the levels.