Weekly Market Outlook 6/1/2025

Hello traders,

Hope you had a great weekend.

You can directly skip to the weekly trade idea or the weekly levels by clicking the links.

Let us recap last week’s ideas.

Realtime Telegram channel +chat access is included with the paid newsletter membership . Click here to subscribe.

Russia-Ukraine Conflict

The conflict between Ukraine and Russia continued to be a significant geopolitical factor, with developments on both the diplomatic and military fronts influencing the broader risk environment.

A. Peace Talk Developments:

Signs of potential diplomatic engagement emerged during the week. Ukraine signaled its readiness to resume direct peace negotiations with Russia, with talks proposed to take place in Istanbul starting Monday, June 2, 2025. However, Kyiv attached a crucial precondition: the receipt of a promised memorandum from the Kremlin clearly outlining Russia's terms and position for ending the more than three-year-long war. Russian officials, including Kremlin spokesman Dmitry Peskov and Foreign Minister Sergei Lavrov, confirmed that a Russian delegation would be prepared to participate in these talks on June 2, with Lavrov stating that Moscow would use the meeting to present its outline for "reliably overcoming" the root causes of the conflict. These proposed talks follow a previous round of direct negotiations held in Istanbul on May 16, which, while not yielding a major breakthrough, did result in an agreement for the largest prisoner exchange of the war. This exchange, involving 1,000 captives from each side, was successfully carried out over the weekend of May 24-25.

B. Military Activity & Claims:

Despite the discussions around peace talks, military activities remained intense, with both sides reporting significant engagements. Ukraine claimed on June 1 to have conducted a "large-scale" drone attack deep into Russian territory. Dubbed "Operation Spider's Web," Ukrainian security officials asserted that the attack, allegedly supervised by President Volodymyr Zelenskyy, successfully destroyed 40 Russian military bombers at airfields including the Belaya air base in Russia's Irkutsk region, over 2,500 miles from Ukraine.

Conversely, Russia launched what Ukraine's air force described as the largest drone and missile barrage since the full-scale invasion began. Ukrainian officials reported that 472 Russian drones were launched, alongside seven missiles. This attack reportedly killed at least 12 Ukrainian soldiers at an army training site located behind the active front line.

Adding to the regional instability, reports emerged over the weekend of explosions causing the collapse of two bridges and the derailment of two trains in western Russia, in regions bordering Ukraine. While the cause of these blasts was not officially stated, they contributed to the heightened sense of insecurity.

C. Market Implications:

The persistent conflict in Ukraine remains a significant underlying source of volatility for global markets. It particularly influences prices for energy commodities, given Russia's role as a major energy exporter, and agricultural products, due to Ukraine's importance as a grain supplier. Broader risk sentiment also remains sensitive to developments in the conflict. Any substantial escalation, such as an expansion of the conflict's scope or the involvement of new parties, or conversely, a tangible de-escalation leading to a credible ceasefire, could trigger more pronounced market reactions.

The juxtaposition of preparations for peace talks with reports of intensified military actions, including major drone attacks claimed by both sides, presents a confusing and concerning picture. While the prospect of dialogue offers a theoretical path towards resolution, the scale and severity of recent military engagements suggest that a swift and peaceful outcome remains elusive. This reality is likely to keep a geopolitical risk premium embedded in relevant asset prices. Markets will probably maintain a degree of skepticism regarding the outcome of the talks unless they are accompanied by a verifiable and significant de-escalation of hostilities on the ground. The risk of miscalculation, accidental escalation, or spillover effects into neighboring regions continues to be a non-negligible concern for global stability and financial markets.

The future of wars is drone attacks with no civilian casualties. Everyone has differing viewpoints over wars but one viewpoint that most would agree is a war with zero human casualties is vastly preferable over all the other outcomes in a war.

The Trade:

Public Companies that are tangentially linked to these drone attacks are

(it’s too soon Algo, noooo don’t go there)

A. AeroVironment (AVAV): Dominance in Tactical UAS and Loitering Munitions

is a top defense stock")

Strategic Focus & Product Relevance: AeroVironment has solidified its position as the U.S. military's foremost supplier of small Unmanned Aircraft Systems (sUAS), including the widely deployed Raven, Puma, and Wasp models. The company is also a globally recognized leader in the design and manufacture of loitering munitions, most notably the Switchblade family. These systems are not only technologically advanced but also extensively combat-proven, directly addressing the critical requirements for tactical ISR and precision strike capabilities that have been so vividly demonstrated and validated in the Ukraine conflict.

Switchblade Loitering Munitions: The Switchblade 300 (anti-personnel) and the larger, more potent Switchblade 600 (anti-armor) are cornerstones of AVAV's portfolio. These systems have been instrumental in Ukrainian defense efforts, supplied via U.S. military aid packages, and have garnered significant international attention for their effectiveness. A key differentiating feature is the "wave-off" capability, allowing operators to abort a mission or re-target an engagement in real-time, thereby minimizing collateral damage and enhancing operational flexibility. The demonstrated success of Switchblade systems has translated into substantial and growing demand from both U.S. and international customers.

Tactical UAS (Puma, Raven): These hand-launched, man-portable systems provide crucial, organic ISR capabilities to ground forces at the tactical edge. The Puma AE, for example, continues to be a system of choice for many allied nations, with recent contracts such as one from the Dutch Ministry of Defence for fleet modernization, underscoring the enduring relevance and upgrade potential of these established platforms.

New Systems Addressing Evolving Battlefield Threats: AeroVironment has demonstrated a commitment to innovation by rapidly developing and launching new systems tailored to the evolving threat landscape:

Red Dragon™: Unveiled in May 2025, Red Dragon is a fully autonomous capable, one-way attack UAS specifically engineered for operation in high-threat, GPS-denied, and communications-degraded environments. Built upon AVAV's common AVACORE™ software architecture and featuring the SPOTR-Edge™ perception system, Red Dragon is designed for rapid development cycles, scalable manufacturing, and modular mission payload integration. This system is a direct response to the intense electronic warfare (EW) challenges and contested airspace scenarios observed in conflicts like Ukraine.

Titan 4: Also launched in May 2025, the Titan 4 is the next generation of AVAV's battle-proven Counter-UAS family. This system enhances capabilities in RF-based detection, classification, and mitigation of hostile drones, addressing a critical operational need in the increasingly drone-saturated modern battlefield.

Strategic Acquisition of BlueHalo: The acquisition of BlueHalo, approved by AVAV stockholders in April 2025 and completed in May 2025, represents a transformative strategic move for the company. Valued at approximately $4.1 billion , BlueHalo is a recognized leader in advanced defense technologies, including AI-driven drone swarms, space systems, directed energy, and cyber capabilities. This acquisition significantly broadens AeroVironment's technological portfolio and market reach, positioning it as a more comprehensive provider of multi-domain autonomous solutions. BlueHalo is anticipated to contribute approximately $170 million in annual revenue and enhance AVAV's access to higher-level defense programs.

Performance & Outlook: AeroVironment's financial performance reflects the strong demand for its solutions and its strategic initiatives.

Fiscal Year 2024 (ended April 30, 2024): The company achieved record revenue of $716.7 million, a substantial 33% increase year-over-year. Net income for FY24 was $60.0 million, translating to a diluted EPS of $2.18. The Loitering Munitions Systems (LMS) segment was a primary catalyst for this growth. The funded backlog at the end of FY24 stood at $400.2 million.

Q1 FY25 (ended July 27, 2024): AVAV reported record Q1 revenue of $189.5 million, up 24% YoY. The LMS segment continued its impressive trajectory with a 68% YoY revenue increase, while the UnCrewed Systems (UxS) segment grew by 22%. Net income for the quarter was $21.2 million. The funded backlog was $372.9 million at quarter-end.

Q2 FY25 (ended October 26, 2024): The company reported record Q2 revenue of $188.5 million, a 4% increase YoY. LMS revenue surged by an exceptional 157% YoY, demonstrating sustained momentum. However, UxS revenue saw a decline of 35% in the quarter. Net income was $7.5 million. The funded backlog grew sequentially to $467.1 million.

Q3 FY25 (ended January 25, 2025): Revenue for the third quarter was $167.6 million, a decrease of 10% YoY, which the company attributed in part to operational disruptions caused by unprecedented high winds and fires in Southern California. Despite the overall revenue dip, the LMS segment continued its growth, with revenue up 46% YoY. UxS revenue declined by 44%. The company reported a net loss of $(1.8) million for Q3. A significant highlight was the achievement of a record funded backlog of $763.5 million, primarily driven by substantial orders for Switchblade and JUMP 20 systems.

Fiscal Year 2025 Full Year Guidance (as of Q3 FY25 earnings release): AeroVironment reaffirmed its revenue guidance for FY25 to be between $780 million and $795 million. The company expects non-GAAP adjusted EBITDA in the range of $135 million to $142 million, and non-GAAP earnings per diluted share between $2.92 and $3.13. This guidance does not yet incorporate the financial impact of the BlueHalo acquisition.

Significant Contract Wins & Program Alignments: AVAV has secured several strategically important contracts. These include a landmark U.S. Army Indefinite Delivery, Indefinite Quantity (IDIQ) contract for Lethal Unmanned Systems with a ceiling value of $990 million and initial funding of $128 million, primarily for Switchblade systems. Other notable wins include a $46.6 million contract from the Italian Ministry of Defence for the JUMP 20 MUAS , a contract with the Dutch Ministry of Defence to modernize its Puma™ UAS fleet , a contract with the German Federal Armed Forces for advanced Uncrewed Ground Vehicles (UGVs) through its Telerob subsidiary , and selection for the Defense Innovation Unit's (DIU) Project Artemis to accelerate the deployment of next-generation autonomous precision munitions. Critically, the Switchblade 600 was selected for Tranche 1 of the U.S. Department of Defense's high-priority "Replicator" initiative, aimed at mass-producing attritable autonomous systems.

Production Capacity Expansion: In response to surging demand, AeroVironment is actively expanding its manufacturing capacity, particularly for Switchblade systems. This includes the establishment of a new production facility in Utah, which is expected to more than double existing Switchblade capacity and support over $500 million in annual Switchblade product revenue in FY25 and beyond, while also providing geographic resiliency.

Bull Case Drivers:

The combat-proven effectiveness and high operational tempo of Switchblade and Puma systems in ongoing conflicts, particularly Ukraine, are driving robust and sustained demand from the U.S. military and international allies.

Strong strategic alignment with key U.S. Department of Defense priorities and procurement initiatives, such as Replicator, LASSO (Low Altitude Stalking and Strike Ordnance), and OPF-L (Organic Precision Fires-Light), ensures a pipeline of significant contract opportunities.

The transformative acquisition of BlueHalo significantly enhances AeroVironment's capabilities in artificial intelligence, autonomy, swarm technology, and extends its reach into the critical multi-domain operational areas of space and cyber warfare.

A rapidly expanding international sales footprint, evidenced by recent contracts from Italy, the Netherlands, Germany, and Lithuania, indicates growing global adoption of AVAV's solutions beyond traditional U.S. markets.

A proactive approach to innovation, demonstrated by the development and launch of next-generation systems like the Red Dragon (specifically designed for GPS-denied environments) and the Titan 4 C-UAS, positions the company to address emerging threats and maintain technological leadership.

Analyst Sentiment (May/June 2025): The consensus among analysts covering AeroVironment in the May/June 2025 timeframe is generally positive, with a predominant leaning towards "Buy" or "Strong Buy" ratings. Zacks Investment Research reported an Average Brokerage Recommendation (ABR) of 1.17 (on a scale of 1-Strong Buy to 5-Strong Sell), indicating a strong buy sentiment, with an average price target of $194.50. Fintel's compilation of analyst forecasts showed an average one-year price target of $187.33. RBC Capital Markets reiterated an "Outperform" rating in May 2025 , and Raymond James upgraded AVAV to "Strong Buy" in April 2025 with a $200 price target. While Public.com data indicated a lower consensus price target of $121.43, this appears to be an outlier or potentially based on a different or older set of analyst inputs. The overall sentiment reflects confidence in AVAV's growth trajectory, driven by its strong market position and alignment with defense modernization trends.

Strategic Evolution and Market Positioning: AeroVironment is undergoing a significant strategic evolution, transitioning from its historical identity as a leading provider of tactical small UAS to becoming a more comprehensive autonomous systems powerhouse. The acquisition of BlueHalo is a cornerstone of this transformation. This move is not merely about augmenting revenue streams but about fundamentally integrating advanced capabilities in artificial intelligence, autonomous swarm logic, and extending AVAV's operational reach into the increasingly interconnected domains of space and cyber warfare. This strategic pivot aligns the company to compete for larger, more complex contracts related to multi-domain operations (MDO) and the U.S. military's vision for Joint All-Domain Command and Control (JADC2). This expanded capability set allows AVAV to address a wider spectrum of modern warfare challenges, moving beyond individual platform sales to offering integrated, intelligent, and networked autonomous solutions.

The intense focus on "attritable" systems—cost-effective platforms designed for use in high-threat environments where losses are anticipated—and the imperative for scalable manufacturing represent another key competitive advantage for AeroVironment in the current geopolitical climate. The lessons from Ukraine have underscored the necessity for large quantities of affordable yet highly capable unmanned systems to sustain operations in a peer or near-peer conflict. AeroVironment's proactive investments in expanding its Switchblade production capacity, including the new Utah facility , and the design philosophy underpinning new systems like Red Dragon, which emphasizes "manufacturing at scale, rapid deployment, and simplified logistics" , directly address this burgeoning demand. This focus on volume and affordability, without compromising critical performance attributes, positions AVAV favorably for large-scale procurement programs such as the DoD's Replicator initiative.

Table: AVAV Flagship Drone Systems & Conflict Relevance

B. Elbit Systems (ESLT): Diversified Global Defense Player with Advanced UAS Capabilities

Strategic Focus & Product Relevance: Elbit Systems Ltd. is a major Israel-based international defense contractor renowned for its broad and technologically advanced portfolio. The company's offerings span airborne, land, and naval systems, command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4I), cyber warfare, ISTAR (Intelligence, Surveillance, Target Acquisition, and Reconnaissance), and electronic warfare (EW) systems. Elbit serves as a primary provider of land-based equipment and Unmanned Aerial Vehicles (UAVs) to the Israeli Defense Forces (IDF), a role that ensures its products are rigorously battle-tested and continuously refined.

UAS Portfolio: Elbit offers a comprehensive range of UAS, from man-portable tactical systems like the Skylark LEX to large, multi-mission platforms such as the Hermes 900.

Hermes 900: This Medium Altitude Long Endurance (MALE) UAV is designed for area dominance, persistent surveillance, intelligence gathering, reconnaissance, and target acquisition operations across both land and maritime domains. Equipped with advanced payloads, the Hermes 900 is operated by over 20 international customers and was notably included in a $335 million contract for a European country, alongside PULS rocket launchers.

Skylark 3 Hybrid: This tactical mini-UAS features an innovative hybrid propulsion system (electric and internal combustion), offering extended endurance of up to 20 hours and the ability to conduct covert operations by flying silently on its electrical engine when over the area of interest. It is designed for division and brigade-level ISTAR missions.

Counter-UAS (C-UAS) Solutions: Recognizing the escalating threat posed by hostile drones, Elbit has developed significant expertise in multi-layered C-UAS solutions. The company recently secured a $60 million contract from a NATO European country for its C-UAS technology, underscoring its capabilities in this critical and rapidly growing market segment.

Other Relevant Systems: Elbit's portfolio includes a wide array of other systems highly relevant to modern warfare scenarios, such as Precision Guided Munitions (PGMs), the Precise and Universal Launching System (PULS) for rockets and missiles, advanced tank ammunition, sophisticated EW self-protection suites for aircraft and vehicles, and the IronBeam high-energy laser defense system (developed in conjunction with Rafael, with Elbit focusing on airborne laser applications). Many of these systems have been operationally proven in recent conflicts.

Performance & Outlook: Elbit Systems has demonstrated robust financial performance, driven by strong global demand for its defense solutions.

Q1 2025 Results (ended March 31, 2025): The company reported impressive first-quarter results, marking its fourth consecutive quarter of double-digit growth. Revenue surged 22% year-over-year to $1.896 billion. GAAP Net Income was $107.1 million, with Non-GAAP Net Income at $117.2 million. This translated to a GAAP EPS of $2.35 and a Non-GAAP EPS of $2.57, which exceeded analyst expectations.

Segment Performance Q1 2025 (YoY growth): Growth was broad-based across Elbit's segments: Aerospace revenue increased by 20% (driven by PGM sales in Israel and Asia Pacific), C4I & Cyber by 12% (radio and command & control systems in Israel and Europe), ISTAR & EW by 4% (Electro-Optic systems in Europe), Land systems by a substantial 48% (ammunition and munition sales in Israel and Europe), and Elbit Systems of America (ESA) by 18% (Warfighter systems and medical instrumentation).

Order Backlog: Elbit reported a record order backlog of $23.1 billion as of March 31, 2025, a 14% increase year-over-year. Approximately 66% of this backlog originates from international markets, and around 51% is scheduled for delivery by the end of 2026, providing strong revenue visibility.

European Market Expansion: Sales to the European market have been a significant growth engine, increasing by 106% from 2021 to 2024. In Q1 2025, Europe accounted for 27% of Elbit's total revenue , reflecting the impact of increased defense spending across the continent.

Key Contracts & "Glocal" Strategy: Recent significant contracts include the aforementioned $335 million European deal for PULS launchers and Hermes 900 UAVs , the $60 million NATO C-UAS contract , and a $57 million contract to supply PULS to Germany. Elbit's "Glocal" (Global/Local) strategy, which involves establishing a strong local presence with subsidiaries and partnerships in key European markets (such as the UK, Germany, Romania, and Sweden), is proving effective in securing contracts and supporting national defense industrial bases. The company also announced recent naval contract wins in May 2025, further expanding its naval defense footprint.

Bull Case Drivers:

A highly diversified product portfolio that addresses a wide spectrum of modern defense requirements, reducing dependence on any single platform or technology.

Strong leverage to the significant increases in European defense budgets and broader global military modernization efforts, driven by heightened geopolitical instability.

An extensive portfolio of combat-proven technologies, rigorously tested and utilized by the Israeli Defense Forces and a growing roster of international customers, providing a critical baseline of reliability and effectiveness.

A substantial and consistently growing order backlog, which provides excellent multi-year revenue visibility and predictability.

A strategic and expanding local presence in key growth markets, particularly in Europe, facilitated by its "Glocal" approach, which enhances market access and supports localization requirements.

Analyst Sentiment (May/June 2025): Analyst sentiment for Elbit Systems in the May/June 2025 period appears more mixed or cautiously optimistic compared to AVAV, though fundamentals are recognized as strong. Jefferies maintained a "Hold" rating on ESLT in May 2025 but increased its price target to $450 from $435, citing sustained international demand driven by rising global defense spending (projecting an additional $280 billion annually from NATO) and Elbit's potential for 10% revenue growth and margin improvement by 2026. Zacks Investment Research reported a single analyst with a "Hold" rating and a $435 price target. SeekingAlpha indicated that, on average, 3 Wall Street analysts rate ESLT as "Neutral". MarketBeat mentioned that Wall Street Zen had cut its rating from "strong-buy" to "buy" in February 2025. Despite the somewhat cautious ratings, analysts acknowledge Elbit's robust performance, particularly the strong Q1 2025 earnings beat, significant backlog, and the operational success of its Land division.

Strategic "Glocalization" and Market Penetration: Elbit Systems' "Glocal" strategy is proving to be a significant competitive differentiator in an international defense market increasingly characterized by industrial nationalism and a desire for sovereign capabilities. As nations prioritize bolstering their domestic defense industries and ensuring security of supply, particularly in Europe , Elbit's approach of establishing and empowering local subsidiaries, fostering local partnerships, and facilitating technology transfer allows it to be perceived more as a domestic contributor than a foreign supplier. This model enhances its ability to win contracts that might otherwise favor purely national champions. This strategy is crucial for long-term market penetration and sustainability, especially as European countries look to "re-arm" and reduce reliance on external defense providers. The company's ability to tailor solutions to specific national requirements while leveraging its global technological expertise provides a compelling value proposition.

The company's broad portfolio, which includes not only UAS but also advanced munitions, electronic warfare systems, C4ISR solutions, and ground vehicle modernizations, positions it to benefit from comprehensive military recapitalization efforts worldwide. The lessons from Ukraine have highlighted the interconnectedness of these capabilities – effective drone operations, for example, rely on robust communications, electronic protection, and precise munitions. Elbit's capacity to offer integrated solutions across these domains, rather than just standalone platforms, is a key strength. The significant growth in its Land segment, driven by ammunition and munition sales , directly reflects the urgent restocking and capability enhancement efforts underway globally in response to the high consumption rates seen in current conflicts.

Table: ESLT Flagship Drone Systems & Conflict Relevance

C. Teledyne Technologies (TDY): Essential Technology Provider through FLIR's Imaging and Sensor Expertise

Strategic Focus & Product Relevance (via Teledyne FLIR Defense): Teledyne Technologies is a highly diversified industrial conglomerate with extensive operations in digital imaging, instrumentation, aerospace and defense electronics, and engineered systems. Its primary relevance to this bull thesis stems from its Teledyne FLIR Defense division, formed after the acquisition of FLIR Systems in May 2021. Teledyne FLIR is a global leader in thermal imaging cameras, sensors, and integrated sensor solutions, as well as select unmanned systems, making it a critical enabler of advanced defense capabilities.

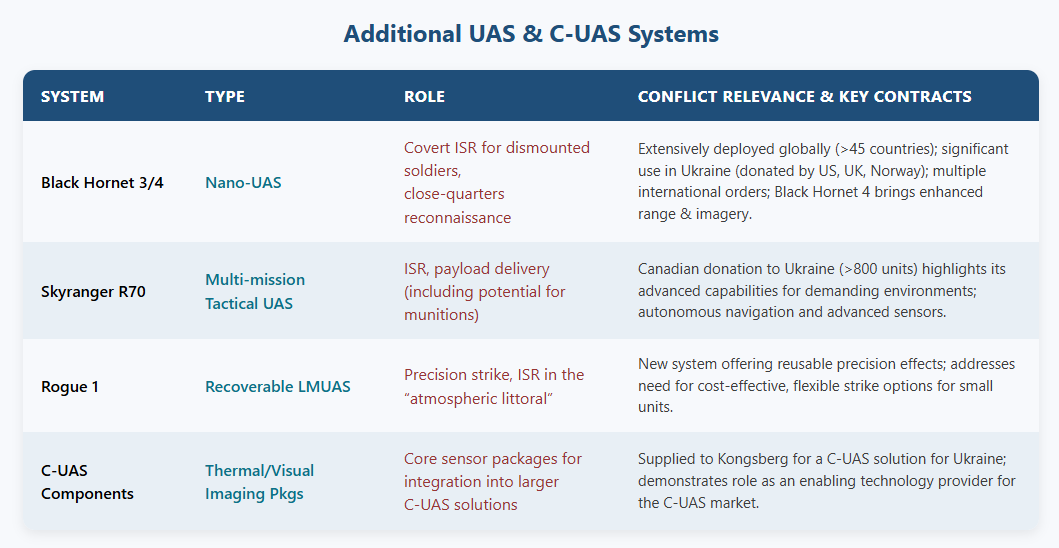

Black Hornet Nano-UAS: The Black Hornet is arguably the world's smallest operational military Unmanned Aerial Vehicle (UAV), providing unmatched covert situational awareness to dismounted soldiers and special operations forces. Weighing just tens of grams, it can be hand-launched and provides real-time video and imagery. It is in service with military and security forces in over 45 countries.

Black Hornet 4: The latest iteration, unveiled in May 2025, features significant upgrades, including a 50% increase in radio communications range (now up to 3 kilometers in optimal conditions), an improved 12-megapixel daytime camera, a higher-resolution thermal imager, enhanced ruggedness (IP52 drone, IP54 ground station), and a new Android tablet ground controller with extended battery life and cold-weather charging capabilities. These enhancements directly address operational feedback and the demands of modern, contested environments.

Ukraine Conflict Context: Black Hornet nano-drones have been donated to Ukrainian forces by several NATO countries, including Norway, the United Kingdom, and the United States, and have reportedly performed successfully in demanding combat conditions, providing invaluable close-in reconnaissance. This battlefield validation further solidifies its market leadership.

Skyranger R70 UAS: This is a more robust, multi-mission tactical UAS featuring autonomous navigation capabilities, advanced thermal and daytime sensors for long-range detection and identification, and a versatile payload capacity of up to 3.5 kilograms, which can include munitions. In a significant endorsement, the Canadian government is donating over 800 Skyranger R70 systems (valued at over CAD$95 million / US$70 million) to Ukraine.

Counter-UAS Involvement: Teledyne FLIR is also contributing to C-UAS solutions by providing advanced thermal/visual imaging systems integrated with highly sensitive radar sensors onto mobile platforms. These are being supplied to Ukraine via a contract with Kongsberg Defence & Aerospace to rapidly identify and track drone threats.

Rogue 1 Loitering Munition: Teledyne FLIR has developed the Rogue 1, a recoverable loitering munition UAS (LMUAS). The company advocates for the advantages of such reusable precision strike systems, particularly for operations in the "atmospheric littoral"—the very low-altitude airspace critical for supporting ground maneuver—as a more cost-effective and flexible alternative to traditional 'One-Way Attack' or FPV drones.

Enabling Technologies (Sensors & Software): Beyond complete UAS platforms, Teledyne FLIR is a crucial provider of core sensor technologies and imaging components. Its Prism™ software, for example, is used for AI-driven object detection, tracking, and autonomous flight control in unmanned platforms, including those being prototyped by companies like Dragoon. This positions Teledyne as a key technology enabler for the broader drone and autonomous systems industry.

Performance & Outlook: Teledyne Technologies has demonstrated consistent growth and profitability, with its defense-related segments contributing significantly.

Q1 2025 Overall Results (ended March 30, 2025): Teledyne reported record Q1 net sales of $1.45 billion, a 7.4% increase year-over-year. GAAP diluted EPS was $3.99, and the company achieved a record non-GAAP diluted EPS of $4.95, surpassing analyst estimates. The company also reported record Q1 GAAP operating margin of 17.9% and non-GAAP operating margin of 22.0%. Teledyne ended the quarter with an all-time record order backlog, with orders exceeding sales for the sixth consecutive quarter.

Aerospace and Defense Electronics Segment (Q1 2025): This segment reported net sales of $242.5 million, a strong increase of 30.6% YoY, with organic sales growth of 7.8%. Operating income for the segment was $55.7 million, up 7.3% YoY. The significant sales increase was primarily driven by defense electronics, which saw sales $57.1 million higher, including $42.3 million from recent acquisitions (notably Qioptiq and Micropac). Management noted that segment margins were temporarily lower due to integration costs associated with these new acquisitions but are expected to improve progressively.

Digital Imaging Segment (Q1 2025): This segment, which includes the bulk of Teledyne FLIR's operations, reported net sales of $757.0 million, an increase of 2.2% YoY. Operating income was $122.3 million, up 7.5% YoY. The sales growth was attributed to higher sales of commercial infrared imaging components and surveillance systems.

Fiscal Year 2025 Full Year Guidance: Teledyne maintained its full-year 2025 non-GAAP EPS outlook in the range of $21.10 to $21.50. The company anticipates achieving approximately $6 billion in total sales for the year.

Bull Case Drivers:

Market leadership in critical sensor and thermal imaging technologies, which are essential components for virtually all advanced UAS, manned aircraft, and ground surveillance systems.

Strong and growing adoption of the Black Hornet nano-UAS by global military forces, with its effectiveness validated in the demanding conditions of the Ukraine conflict, driving repeat orders and new customer interest.

The Skyranger R70 tactical UAS is gaining significant traction, highlighted by the substantial order from Canada for donation to Ukraine, indicating its suitability for modern battlefield requirements.

Strategic positioning as a key enabler of the broader drone ecosystem through the provision of advanced sensors, AI-driven software, and imaging payloads to other defense contractors and system integrators.

A well-diversified overall business model provides financial stability and resilience, while the defense-relevant segments (Aerospace & Defense Electronics, parts of Digital Imaging) are experiencing robust growth driven by current geopolitical trends.

Analyst Sentiment (May/June 2025): Analyst sentiment for Teledyne Technologies in the May/June 2025 period is predominantly positive, with a consensus leaning towards "Strong Buy" or "Buy." Zacks Investment Research reported an Average Brokerage Recommendation (ABR) of 1.33 (on a scale of 1-Strong Buy to 5-Strong Sell) based on nine analysts, with seven of those issuing "Strong Buy" ratings. The average price target from these analysts was $555.11. Stockinvest.us noted a bullish technical pattern (rectangle formation) predicting a potential rise to $564.94 and highlighted rising volume with price increases as a good technical signal. Analysts generally view Teledyne's diversified portfolio, strong execution, and strategic acquisitions favorably.

Teledyne as a Foundational Technology Provider: Teledyne Technologies, particularly through its FLIR division, functions as a critical "arms dealer to the drone revolution" by supplying essential sensor and imaging technology. While the company produces its own highly successful UAS platforms like the Black Hornet and Skyranger R70, its core expertise in thermal imaging, advanced electro-optical sensors, and AI-enabled image processing software makes it a vital supplier to a much broader segment of the defense and industrial markets, including other drone manufacturers and system integrators. This role as a foundational technology provider offers a diversified revenue stream within the rapidly expanding UAS market. As the entire unmanned systems sector grows, the demand for these critical sub-systems—the "eyes and brains" of autonomous platforms—will also increase, irrespective of which specific drone airframe or prime contractor wins a particular program. This strategic positioning provides Teledyne with a degree of insulation from the platform-specific competition while allowing it to benefit from the overall market uplift.

The company's consistent investment in R&D and strategic acquisitions, such as FLIR itself and more recently Qioptiq (specializing in optical components and systems) , continually strengthens its technological leadership and market reach. The ability to provide high-performance, ruggedized sensor solutions suitable for demanding military applications, from individual soldier systems to sophisticated airborne and maritime platforms, ensures Teledyne remains at the forefront of defense modernization efforts globally. The increasing emphasis on data fusion, AI at the edge, and networked operations further plays to Teledyne's strengths in providing intelligent sensing solutions.

Table: TDY (FLIR) Flagship Drone Systems & Conflict Relevance

Comparative Analysis & Strategic Positioning

A comparative look at AeroVironment, Elbit Systems, and Teledyne Technologies reveals distinct market positions, financial scales, and strategic approaches, yet all are poised to benefit from the overarching trends in drone warfare and increased defense spending.

Distinct Competitive Advantages and Market Niches:

AeroVironment (AVAV): AVAV excels as a specialist in tactical, man-portable UAS and cutting-edge loitering munitions. Its deep-rooted relationships with the U.S. Army and Special Operations Command (SOCOM) provide a strong domestic base. The company is characterized by its agility and innovation in developing rapidly deployable and combat-effective solutions. The recent acquisition of BlueHalo is a strategic move to significantly bolster its capabilities in AI, autonomy, and multi-domain systems.

Elbit Systems (ESLT): Elbit is a broad-spectrum international defense prime with deep integration within the Israeli defense ecosystem, which serves as a demanding proving ground for its technologies. The company has a rapidly expanding presence in Europe and other international markets. Its key strengths lie in offering comprehensive, integrated solutions that span platforms (air, land, sea), C4ISR, EW, and C-UAS. Elbit's "Glocal" strategy, focusing on local industrial participation and partnerships, is a significant facilitator of market access in an era of increasing defense industrial nationalism.

Teledyne Technologies (TDY): Through Teledyne FLIR, TDY is a technology leader in advanced sensors, thermal imaging, and digital imaging solutions. It dominates the nano-UAS segment with its Black Hornet system. Crucially, Teledyne acts as a key enabling technology provider for the wider defense industry, supplying critical components and sub-systems to other prime contractors and UAS manufacturers. Its highly diversified overall business model offers a degree of insulation from the cyclicality sometimes associated with pure-play defense companies.

Synergies and Interplay: While these three companies operate as competitors in certain segments, the defense market is also characterized by complex interdependencies and opportunities for collaboration. For instance, Teledyne FLIR's advanced sensors and imaging payloads could potentially be integrated into platforms developed by AeroVironment or Elbit Systems. The overarching trend in modern defense is towards integrated, multi-domain systems that require contributions from a wide array of specialized technology providers. This environment may foster further strategic partnerships, joint ventures, or even mergers and acquisitions as companies seek to consolidate capabilities and offer more comprehensive solutions. The demand for interoperability and open architectures could also drive collaboration.

Differing Investment Profiles: The three companies present distinct risk/reward profiles and varying degrees of exposure to the core drone warfare theme. AeroVironment offers a more concentrated, pure-play investment in tactical UAS and loitering munitions. This focus can lead to higher growth potential, particularly as these specific capabilities are in high demand, but it may also entail greater volatility linked to program wins and geopolitical events. Elbit Systems, as a large, diversified international defense prime, provides broader exposure to the general uplift in global defense budgets, with UAS forming one key component of its extensive portfolio. Its large and growing backlog suggests a degree of revenue stability and predictability. Teledyne Technologies offers exposure to the drone market primarily through its critical enabling technologies (sensors, imaging) and its specialized UAS platforms (Black Hornet, Skyranger). The company's broader industrial and commercial technology businesses provide significant diversification, potentially moderating the impact of defense-specific market fluctuations.

These differing profiles are also reflected in their valuation metrics. AeroVironment often commands a higher price-to-earnings (P/E) multiple, indicative of investor expectations for strong growth in its LMS segment and its overall market position. Elbit Systems' valuation has been strengthening, supported by its robust financial performance, substantial backlog growth, and successful expansion into the European market. Teledyne's P/E ratio tends to be more in line with those of diversified industrial technology companies, reflecting its broader business mix. These valuation disparities underscore the market's perception of their respective growth stages, risk profiles, and the specific sub-segments of the defense and technology markets they address.

VI. Investment Risks & Considerations

While the bull thesis for AVAV, ESLT, and TDY is compelling, investors must consider several risks inherent in the defense industry and specific to these companies:

Dependence on Government Defense Spending: The revenues and growth prospects of all three companies are significantly tied to government defense budgets and procurement priorities in the U.S. and internationally. Unforeseen changes in the geopolitical landscape, shifts in national defense strategies, or specific program cancellations or delays due to budgetary constraints can materially impact financial performance and backlog.

Technological Obsolescence & Intense Competition: The drone and defense technology markets are characterized by rapid innovation and intense competition. Failure to invest adequately in R&D, anticipate evolving threats, or counter emerging technologies (such as increasingly sophisticated EW systems or very low-cost, mass-produced FPV drones from new entrants) could lead to technological obsolescence and an erosion of market share. The "democratization of air power" also implies lower barriers to entry for agile and disruptive competitors.

Contract Execution & Supply Chain Risks: Scaling production to meet surge demand, as seen with AeroVironment's Switchblade capacity expansion , can strain supply chains, lead to component shortages , and introduce execution risks related to quality control, cost overruns, and delivery schedules. Disruptions in the global supply chain for critical electronic components or raw materials can impact production timelines and profitability.

Mergers & Acquisitions (M&A) Integration Risks: Large-scale acquisitions, such as AeroVironment's recent $4.1 billion deal for BlueHalo and Teledyne's earlier acquisition of FLIR Systems and more recent acquisition of Qioptiq , carry inherent integration risks. These include challenges in harmonizing corporate cultures, retaining key personnel, achieving projected synergies, and managing potential antitrust scrutiny. Failure to integrate acquisitions successfully can dilute shareholder value and distract management.

Geopolitical Event Specificity & Customer Concentration: Over-reliance on demand generated by a single conflict or a limited number of major customers can introduce volatility. For example, AeroVironment noted a "transition year pivoting away from Ukraine demand" in some respects for FY25, highlighting the need to diversify. While the current geopolitical climate suggests sustained high demand, a sudden de-escalation or shift in regional priorities could impact order flow. Diversification of customers, geographic markets (as pursued by Elbit ), and product applications is crucial for mitigating this risk.

Valuation Sensitivities: Defense technology stocks can trade at premium valuations during periods of heightened geopolitical tension and strong market demand. Investors need to carefully assess whether current and projected growth prospects adequately justify these multiples, as valuations can be sensitive to changes in market sentiment or growth expectations.

Ethical Considerations and Export Controls: The development and proliferation of autonomous and lethal drone systems raise significant ethical questions regarding their use in warfare, particularly concerning autonomous decision-making in targeting. These concerns can lead to increased public scrutiny, calls for tighter regulation, and more stringent export controls imposed by governments, potentially limiting market access for certain advanced systems or sales to specific countries. Elbit Systems, for instance, has faced protests and divestment actions by some international investment firms due to its involvement in the Israeli-Palestinian conflict.

Economic Data for the upcoming week:

The week of June 2 - June 8 is poised to be particularly data-sensitive, with several high-profile releases and events capable of significantly influencing market direction.

U.S. Jobs Report (Nonfarm Payrolls - NFP): This is arguably the most critical data point of the week, scheduled for Friday. The consensus forecast points to a moderation in job creation to 130,000 in May, down from April's 177,000. The unemployment rate and wage growth figures (Average Hourly Earnings) will also be intensely scrutinized for signs of labor market tightness and inflationary pressures. A result that deviates substantially from expectations – either much stronger, suggesting persistent economic resilience and inflationary risk, or much weaker, signaling a cooling economy – could provoke a sharp repricing of Federal Reserve rate cut expectations and drive considerable volatility across equities, bonds, and the U.S. dollar.

ISM Purchasing Managers' Indexes (PMIs): The ISM Manufacturing PMI (Monday) and the ISM Services PMI (Wednesday) will offer crucial insights into the health and momentum of these key sectors of the U.S. economy during May. The manufacturing sector has been showing signs of contraction (previous reading 48.7, with 50 being the dividing line between expansion and contraction ), and the services sector, while still expansionary (previous reading 51.6 ), will be watched for any signs of slowing. These reports are also valuable for indications of price pressures and the potential impact of tariffs on business activity and sentiment.

Central Bank Decisions (Bank of Canada & European Central Bank):

The Bank of Canada (BoC) announces its interest rate decision on Wednesday. While no specific change is universally forecast in the provided snippets, the policy statement and any forward guidance will be important for the Canadian dollar and could influence broader sentiment regarding the global monetary policy cycle.

The European Central Bank (ECB) is widely expected to cut its deposit rate by 0.25 percentage points to 2.00% on Thursday. Given that this cut is largely anticipated and priced in by markets, the focus will be squarely on President Christine Lagarde's press conference and the ECB's updated macroeconomic projections. Any signals regarding the likelihood and timing of future rate cuts, or concerns about inflation persistence or economic growth, will be key drivers for the Euro and European markets. The ECB's assessment of trade and tariff uncertainty will also be of interest.

Ongoing Tariff Narrative: While no specific tariff deadlines fall within this week (the U.S.-EU tariff deadline was pushed to July 9 ), any new pronouncements, negotiation updates, or retaliatory actions related to U.S. trade policy with the EU, China, or other partners will continue to be a source of market sensitivity.

WEEKLY LEVELS:

Subscribers are urged to use the tradingview indicator to plot the levels.