Weekly Market Outlook 6/16/2025

FOMC WEEK

Hello traders,

I hope you all had a great weekend.

Wishing all Fathers a joyful and Happy Father’s Day and hope you enjoy your day.

Let us recap trade ideas from last week.

Realtime Telegram channel +chat access with intraday orderflow summaries is included with the paid newsletter membership . Click here to subscribe.

THIS PAST WEEK: TALE OF TWO HALVES

The week of June 9, 2025, will be etched in traders' memories as a brutal lesson in the fragility of market sentiment. It was a period that began with a surge of risk-on optimism, fueled by a potent cocktail of cooling inflation data and an apparent de-escalation in the U.S.-China trade war. By midweek, bond yields were tumbling, and equity indices were confidently probing psychological milestones, with the S&P 500 flirting with the 6,000 level for the first time since February. The narrative was clear: the Federal Reserve, seeing inflation pressures recede, would finally have the green light to pivot towards a more dovish monetary policy, unleashing a fresh wave of liquidity into the financial system.

This carefully constructed bullish thesis was shattered in the globex session of trading on Thursday, June 12. News of Israeli military strikes against Iranian nuclear facilities, followed by swift Iranian missile retaliation, sent a violent shockwave across global markets. The placid, risk-on environment evaporated in an instant, replaced by a classic flight to safety. Equities plunged, with the Dow Jones Industrial Average shedding more than 700 points, erasing its weekly gains. Crude oil prices, which had been languishing under the weight of weak demand signals, exploded higher in a geopolitical panic, with West Texas Intermediate (WTI) futures surging more than 7%. The CBOE Volatility Index (VIX) jolted back above 20, a stark quantitative measure of the sudden rush for portfolio protection.

The market's abrupt and violent reversal exposed just how complacent investor positioning had become. The early-week news flow provided a textbook setup for a sustained rally, likely drawing in momentum traders and encouraging a significant build-up of long positions in equities and other risk assets. The soft Consumer Price Index (CPI) and Producer Price Index (PPI) reports directly challenged the "higher-for-longer" interest rate narrative that had capped market enthusiasm for months. Simultaneously, the announcement of a U.S.-China trade "framework" in London, while light on new details, appeared to remove a significant tail risk that had been a persistent source of anxiety.

The combination of these two powerful catalysts created a potent, if ultimately illusory, bullish signal. The sudden, exogenous shock from the Middle East acted as a devastating trigger for a rapid and painful unwinding of these crowded trades. The market's foundation, it turned out, was far more fragile than the calm trading of early June suggested. It proved acutely susceptible to headline risk, a vulnerability that now defines the path forward.

Investors are now caught in a vicious cross-current. On one side is the improving macroeconomic backdrop, where disinflation appears to be taking hold. On the other is a dangerously escalating geopolitical landscape that threatens to unleash a stagflationary shock: higher energy prices and slower global growth. The week ahead, dominated by a critical Federal Reserve policy meeting, will be a test of whether the underlying macro-optimism can reassert itself or if geopolitical fear will now dictate the market's every move.

The Inflation Question: A Fleeting Glimmer of Hope?

For a brief, tantalizing moment, the week's economic data offered a vision of a post-inflationary world. A pair of reports from the Bureau of Labor Statistics (BLS) on consumer and producer prices suggested that the Federal Reserve's long and arduous battle against inflation was finally bearing fruit, providing the central bank with the flexibility it desperately needed to consider easing its restrictive monetary policy. This narrative, however, now stands overshadowed by a new inflationary threat emanating from the geopolitical arena.

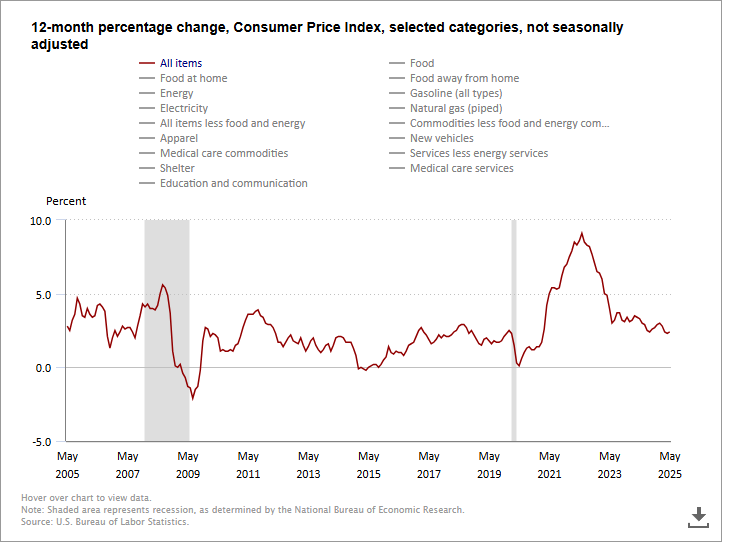

The Consumer Price Index (CPI) Deconstructed (May Data)

The main event on the economic calendar was the May CPI report, released on Wednesday, June 11. The data was unequivocally softer than anticipated, sparking an immediate rally in both stocks and bonds.

The headline Consumer Price Index rose just 0.1% month-over-month (MoM), below the consensus forecast of 0.2%. On a year-over-year (YoY) basis, headline inflation held at 2.4%, in line with expectations but showing no signs of re-acceleration.

The real story, however, was in the core figures, which strip out volatile food and energy prices and are more closely watched by the Fed as a signal of underlying inflation trends. Core CPI rose a mere 0.1% MoM, a significant miss from the +0.3% expected. This brought the YoY core inflation rate down to 2.8%, also undershooting the 2.9% consensus forecast. This "core miss" was the primary catalyst for the market's initial bullish reaction, as it suggested that the stickier components of inflation were finally starting to break.

A deeper dive into the report's components reveals a complex picture:

Energy as a Disinflationary Force: A key driver of the soft headline print was a 1.0% monthly decline in the energy index. Gasoline prices fell a notable 2.6% in May, providing relief to consumers at the pump. This trend, however, is now under direct threat. The surge in crude oil prices following the Middle East conflict on Friday ensures that energy will become a significant inflationary force in the June CPI report.

Stubborn Shelter Costs: The shelter index, which accounts for a substantial portion of the CPI basket, continued its relentless climb, rising 0.3% over the month. Both owners' equivalent rent (+0.3%) and rent of primary residence (+0.2%) posted increases, highlighting that this crucial component of services inflation remains stubbornly persistent, even as it moderates from its peak.

The Goods vs. Services Dichotomy: The report continued to show a divergence between goods and services inflation. While services inflation remains elevated, driven by shelter and labor costs, the progress on core goods inflation appeared to stall or even reverse slightly. This was a point of specific concern raised by Fed Governor Adriana Kugler in a speech just days before the report's release, where she warned that this reversal could be exacerbated by tariffs.

Rising Food Costs: The food index rose 0.3% MoM, with the index for food at home increasing 2.2% over the past year. This directly impacts household budgets and consumer sentiment, and could be further pressured by supply chain disruptions.

The Producer Price Index (PPI) Confirmation (May Data)

The Producer Price Index report, released on Thursday, June 12, largely corroborated the benign message from the CPI. The final demand PPI edged up just 0.1% in May, following a 0.2% decline in April, and the YoY figure came in at 2.6%, precisely in line with expectations. This data suggested that price pressures at the wholesale level were well-contained.

A more granular look at the intermediate demand data provided further evidence of disinflation in the production pipeline. Prices for unprocessed goods for intermediate demand fell 1.6%, led by a sharp 3.5% drop in energy materials. While prices for processed goods ticked up 0.1%, the overall trend pointed towards moderating input costs for businesses.

Taken together, the CPI and PPI reports for May painted a picture of an inflation rate that was steadily, if slowly, converging on the Fed's 2% target. This bolstered the case for the Fed to adopt a more dovish tone at its upcoming meeting and increased market-implied probabilities of a rate cut later in 2025, sending Treasury yields tumbling mid-week.

Yet, a shadow looms over this optimistic interpretation. The May inflation data is, by its nature, a backward-looking indicator. It was collected before the full impact of the Trump administration's latest round of tariffs could filter through the economy and, most critically, before the geopolitical explosion in the Middle East sent oil prices screaming higher.

Fed Governor Kugler provided a prescient warning in her June 5 speech, noting that research showed a quick pass-through of tariffs into consumer prices and that the reversal in core goods inflation was a worrying sign. Analysts have echoed this concern, suggesting that companies may have been front-loading imports and drawing down inventories to temporarily absorb the initial tariff costs, masking the true inflationary impact.

The "good news" on May inflation may therefore represent a temporary calm before a new storm. The combination of the new 55% tariff on a wide range of Chinese goods, the 50% tariff on steel and aluminum, and now a major oil price shock creates a potent recipe for a re-acceleration of inflation in the June and July reports. This presents an extraordinarily difficult challenge for the Federal Reserve, potentially forcing it to confront a stagflationary environment that undermines the entire "Fed pivot" narrative that so powerfully drove markets for the first half of the week.

The Geopolitical Cauldron: Twin Conflicts and a New Trade Order

While macroeconomic data and central bank policy typically dominate market discourse, the past week was a stark reminder that geopolitics can hijack the narrative without warning. A sudden, violent escalation in the Middle East, the persistent grind of the war in Ukraine, and the delicate recalibration of global trade relationships formed a complex and volatile backdrop that ultimately dictated the week's market outcomes.

Middle East on the Brink: The Week's Dominant Catalyst

The market's focus shifted seismically on Friday, June 13, with reports of Israeli airstrikes targeting Iranian nuclear facilities and key military personnel. The move was a dramatic escalation in the long-simmering shadow war between the two regional powers. Iran's response was swift, launching a barrage of missiles toward Israel, raising the specter of a full-blown regional conflict.

The market reaction was immediate and severe:

Energy Prices Explode: WTI crude oil futures, the U.S. benchmark, surged more than 7% to close at $72.98 per barrel, having touched an intraday high of $77.62, a level not seen since January. The price spike reflected fears of a major disruption to global oil supply. The Middle East is home to several of the world's top producers, including Saudi Arabia, Iraq, and Iran itself. A wider conflict could threaten not only production facilities but also critical maritime chokepoints like the Strait of Hormuz, through which a significant portion of the world's oil flows.

Equities Tumble: Global stock markets plunged on the news. The Dow Jones Industrial Average fell over 700 points, and the S&P 500 reversed its weekly gains. The sell-off was broad-based, but certain sectors were hit particularly hard. Travel-related stocks, such as airlines and hotels, declined on the prospect of higher fuel costs and reduced global travel.

Sector Rotations: Conversely, defense and energy stocks rallied. Major defense contractors like Northrop Grumman (NOC) and Lockheed Martin (LMT) saw their shares jump more than 3%. Oil producers like Occidental Petroleum (OXY) and oil majors like Exxon Mobil (XOM) also posted strong gains, tracking the surge in crude prices.

The Grinding War in Ukraine: A Persistent Risk Factor

While overshadowed by the drama in the Middle East, the war in Ukraine continued its brutal course, remaining a significant source of global instability. The week saw Russia launch another massive wave of drone and missile attacks against Ukrainian cities and infrastructure, with Kyiv reporting a record barrage of nearly 500 drones on June 9 alone. On the ground, Russian forces continued to make incremental advances in the Sumy and Donetsk regions as part of their strategy to create a "buffer zone" along the border.

The dynamics of international support for Ukraine are also in flux. While European allies like Germany and the Netherlands pledged new aid packages, the U.S. administration signaled its intention to curtail future support, a major strategic shift that could have profound consequences for the war's trajectory. This persistent conflict provides a structural floor for energy and agricultural commodity prices and serves as a constant reminder of the fragility of the post-Cold War global order.

The New Trade Order: A Fragile U.S.-China Truce

Early in the week, markets were buoyed by news that U.S. and Chinese negotiators in London had agreed on a "framework" to resolve their escalating trade disputes. The deal appeared to walk both nations back from the brink of a full-blown trade embargo.

The key terms of the framework included:

Tariff Reductions: The U.S. agreed to lower its punitive tariffs on Chinese goods from a peak of 145% down to 55%. In return, China would reduce its retaliatory tariffs on U.S. goods to 10%.

Rare Earths and Visas: Critically, China committed to resuming the export of rare earth minerals, which are vital for U.S. technology and defense industries and had been severely restricted. The U.S., in turn, agreed to walk back threats to aggressively revoke visas for Chinese students.

However, the market's reaction was notably subdued. Investors and analysts interpreted the deal not as a genuine breakthrough, but rather as a necessary implementation of the fragile "Geneva truce" reached in May, designed to prevent a complete collapse in relations. The remaining 55% U.S. tariff is still considered highly damaging and a significant drag on global trade. Furthermore, this was happening in the context of the Trump administration's broader trade agenda, which saw 50% tariffs on steel and aluminum imposed on most trading partners, including key allies, on June 4.

The week's events vividly illustrate the interconnected nature of modern geopolitical risk. The surge in oil prices caused by the Israel-Iran conflict, for instance, directly benefits Russia by boosting its state revenues, thereby strengthening its ability to sustain its war effort in Ukraine. The U.S. commitment to supply China with advanced technology in exchange for rare earth minerals highlights a deep strategic interdependence that complicates the narrative of pure competition. For investors, the lesson is clear: geopolitical events can no longer be analyzed in isolation. A flare-up in one corner of the globe can have immediate and cascading consequences for markets and strategic calculations worldwide, ushering in a new era of complexity and volatility.

The Week Ahead: Navigating the FOMC and Geopolitical Fallout (June 16-20)

As investors attempt to process the aftershocks of the past week's geopolitical earthquake, their attention will immediately pivot to a packed economic calendar dominated by the Federal Reserve's monetary policy meeting. The interplay between the Fed's forward guidance and the relentless stream of headlines from the Middle East will determine the market's next directional move.

The Main Event: FOMC Decision (June 17-18)

All eyes will be on the Federal Open Market Committee this week. While a decision to hold the federal funds rate steady in its current range of 4.25%-4.50% is a near certainty, the meeting's true significance lies in the signals it sends about the future path of monetary policy.

The Dot Plot: The most scrutinized element of the release will be the Summary of Economic Projections (SEP), which includes the "dot plot" illustrating individual members' expectations for the policy rate. Before the recent turmoil, the market was hoping the soft inflation data would lead to a dovish shift, with the median dot perhaps signaling multiple rate cuts in 2025. Now, the committee must weigh that disinflationary impulse against the new inflationary threat from the oil shock and tariffs. A dot plot that shows fewer cuts or a higher median rate for year-end would be interpreted as hawkish and would likely send risk assets lower.

Powell's Press Conference: Fed Chair Jerome Powell's press conference following the announcement will be the week's most critical event. He will face a barrage of questions attempting to decipher the Fed's reaction function in this new, complex environment. Key questions will include:

How does the Fed reconcile the soft May inflation data with the clear and present inflationary danger from the Middle East conflict and tariffs?

Does the committee view the potential energy price spike as a "transitory" shock it can look through, or a "persistent" threat that requires a hawkish policy response?

What is the Fed's updated assessment of the inflationary impact from the new U.S. trade policy regime?

How has the balance of risks to the dual mandate, achieving maximum employment and stable prices has shifted since the last meeting? Powell's tone and emphasis will be parsed for any hint of a tilt towards prioritizing inflation-fighting over supporting growth, or vice-versa.

Other Key Data

Beyond the Fed, Tuesday's Retail Sales report for May will provide a vital check on the health of the U.S. consumer. A strong number would suggest the economy remains resilient, potentially giving the Fed more room to stay hawkish. A weak number, conversely, would raise fears of a slowdown and increase pressure on the Fed to cut rates.

WEEKLY LEVELS

Subscribers are urged to use the tradingview indicator to plot the levels.

NOTE: Paid Subscribers will receive September Contract Levels by Tuesday EOD.