Weekly Market Outlook 6/29/2025

Short weak Shorts weak(reusing subtitles stage of the market)

Hello traders,

Hope you all had an amazing weekend with perfect weather and spending time with your loved one(s).

We are squarely in the middle of Low volatility Summer action right now.

Last week, we had a rather nondescript week on indices but ended up scoring a home run on the Drone basket and a CL knife catch for about 200 ticks.

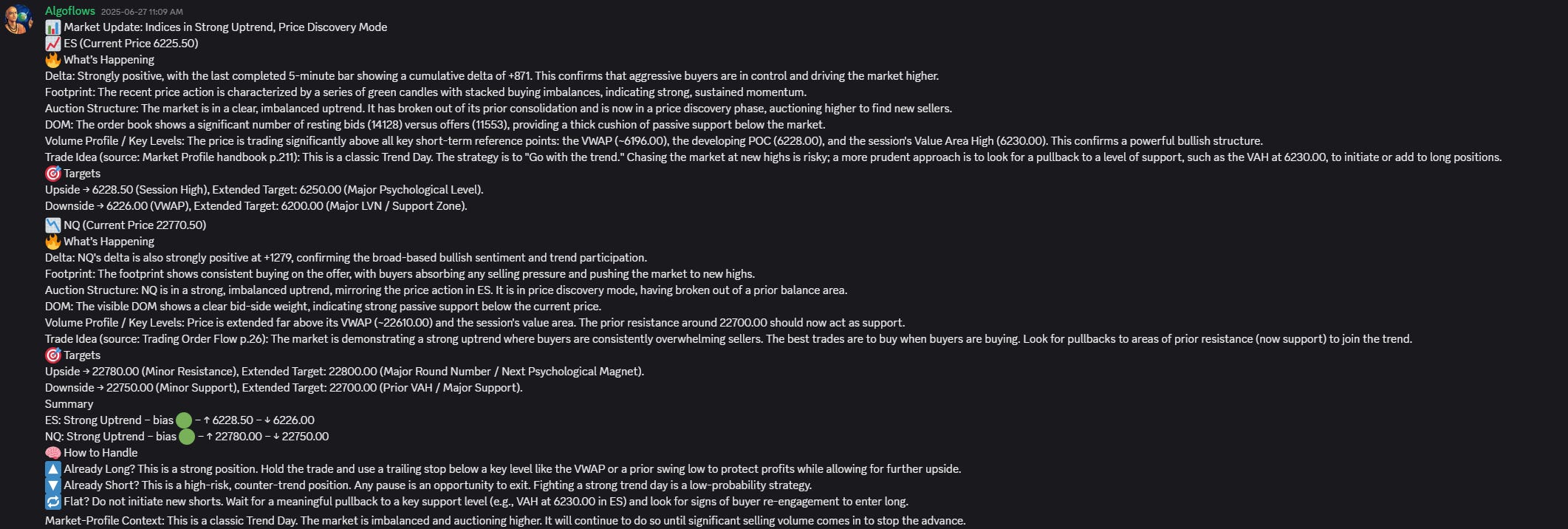

Speaking of Discord, we have added more features to the Discord with real-time orderflow summaries being beamed in everyday for ES and NQ traders. We are in the process to add the same for other instruments in the upcoming weeks.

90% of this plan is free and only the weekly levels are paywalled. Realtime Discord access with intraday orderflow summaries is included with the paid newsletter membership . Click here to subscribe.

The Rare Earths Accord: A Fragile Truce

A wave of market optimism followed the formal announcement of a new trade-agreement framework between Washington and Beijing. After a series of high-level talks in London and Geneva, the two countries reached an accord meant to defuse a tariff conflict that had pushed duties as high as 145 percent on Chinese goods and 125 percent on American goods.

The centerpiece of the deal, outlined by U.S. Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick, is China’s pledge to accelerate shipments of rare-earth minerals and magnets to the United States. These inputs are critical for American automotive, semiconductor, and defense manufacturers, all of which faced supply-chain risks after Beijing slowed exports in retaliation for earlier U.S. tariffs.

In exchange, the United States will roll back several restrictions it had placed on China. Details are sparse, but the concessions are expected to include lighter export curbs on certain technologies and materials that Chinese industries need.

Officials keep describing the arrangement as a “framework” and an “additional understanding” that extends a prior 90-day pause on new tariff hikes. That pause expires on 9 July, so the current deal functions more like a tactical cease-fire than a lasting settlement. The immediate threat of a full tariff war has been averted, yet the fundamental strategic disputes remain. Markets are cheering the absence of an immediate storm, but the long-term outlook is still unsettled.

The Chip Sector’s Relief Rally: Short-Term Gain, Long-Term Questions

No segment reacted more strongly to the truce than semiconductors. Shares of Nvidia, Taiwan Semiconductor Manufacturing, Advanced Micro Devices, and Qualcomm all advanced, highlighting the sector’s exposure to U.S.–China tensions. The rally reflects two immediate benefits: restored access to Chinese rare earths, essential for chip production, and reduced odds of tariffs on finished electronics such as servers and laptops that rely on U.S.-designed chips but are assembled in China.

Beneath the bounce lies a tougher reality. The U.S.–China dispute has shifted from tariffs to a broader technology contest. Washington’s stated objective is to preserve a wide lead in fields such as artificial intelligence and advanced computing, and that aim is enforced through tight export controls that limit China’s access to cutting-edge semiconductors and the tools required to build them.

Semiconductor companies are acting on the assumption that this strategic rivalry will deepen. Spurred by geopolitical risk and backed by large subsidy programs like the U.S. CHIPS Act plus similar initiatives in Europe and Japan, firms are adopting “second-sourcing” or “China plus one” supply-chain models. They are spending billions on new fabrication plants in Arizona, Ohio, Japan, and several European locations, a multi-year effort to reduce dependence on any single region, especially Taiwan and mainland China.

The contrast is stark. Equity markets are rewarding a short-term détente that boosts margins and eases logistics pressures, while the industry allocates capital for a future defined by persistent fragmentation and political complexity. The current rally may be ignoring the full cost and difficulty of operating in a permanently divided global tech landscape.

NON-FARM PAYROLL CONUNDRUM

This week is going to be a short week with Non-Farm Payrolls being moved up to Thursday and JOLTS and ISM PMI on Tuesday alongwith Chair Powell’ speech.

The forecasts suggest another month of contraction for the manufacturing sector (a reading below 50) and a labor market that is moderating from the red-hot pace of previous years. The headline non-farm payrolls (NFP) forecast of +129,000 would be a step down from May's +139,000 reading and well below the averages seen in 2023 and 2024, while the unemployment rate is expected to hold steady at a still-low 4.2%.

The market's reaction will hinge on how the actual NFP data deviates from these consensus expectations. Three primary scenarios exist:

Scenario 1: Hotter Than Expected. A headline NFP number significantly above 175,000, especially if paired with an upside surprise in average hourly earnings (e.g., +0.4% or higher), would directly challenge the narrative of a cooling labor market. This would force the market to price out the probability of near-term Fed rate cuts. The likely reaction would be bearish for bonds (yields would rise sharply), bearish for equities (as the prospect of "higher for longer" rates would weigh on valuations), and bullish for the U.S. Dollar.

Scenario 2: In-line with Consensus. A report that lands close to the consensus forecasts of +129k jobs and a 4.2% unemployment rate would largely confirm the current "soft landing" narrative. It would signal a labor market that is cooling but not collapsing, giving the Fed little reason to deviate from its current "wait-and-see" approach. The market reaction in this scenario could be relatively muted, as it is the outcome that is most heavily priced in.

Scenario 3: Weaker Than Expected. A headline NFP number significantly below 100,000, particularly if accompanied by a surprise uptick in the unemployment rate, would amplify fears of a more rapid economic slowdown or recession. This would increase the probability of more aggressive Fed rate cuts. The initial market reaction would likely be bullish for bonds (yields would fall), bullish for equities (the classic "bad news is good news" reaction, as it brings the Fed closer to easing), and bearish for the U.S. Dollar. However, a disastrously weak number (e.g., negative payrolls) could flip this sentiment, sparking outright recession fears and triggering a broad "risk-off" move where both stocks and bond yields fall together.

JESUS ALGO, YOU HAVE TURNED INTO IF-THEN-THIS-THAT GUY.

Okay, gun to my head prediction, my models predict you can trim most longs this week and start medium term shorts on overextended beta.

Exactly which overextended names Algo?

*CLIFFHANGER*

I will send out a report midweek with companies and positioning.

Sneak Peek into the report:

Keep your eyes peeled for the email drop this week.

WEEKLY LEVELS:

Subscribers are urged to use the tradingview indicator to plot the levels.

NOTE: SUBSCRIBERS ARE URGED TO JOIN THE DISCORD AT THEIR EARLIEST CONVENIENCE.

Discord link here: