Weekly Market Outlook 7/13/2025

Inflate this Donny

Hello traders,

Last week crawled along at peak boredom pace. Directional futures trades handed us tiny targets, a typical summer snooze fest, but hey, at least the sun’s out.

NEW: AUDIO SUMMARY OF THIS ARTICLE HERE, CLICK ON PLAY FOR THOSE WHO DO NOT LIKE TO READ.

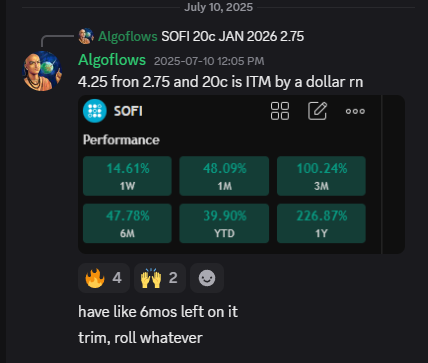

Recap of last week’s select trades:

90% of this plan is free and only the weekly levels are paywalled. Realtime Discord access with intraday orderflow summaries is included with the paid newsletter membership . Click here to subscribe.

Our swing idea on SOFI 0.00%↑ is up almost a 100% in a couple weeks with about 6 months left on the trade.

The Tariff Tightrope and the AI Boom: Markets Split Ahead of Inflation Data

Global risk assets are trapped in a bifurcated narrative. Artificial-intelligence euphoria props up US megacap technology and Bitcoin, while a sharp pivot toward protectionism and fresh geopolitical flare-ups pressure cyclicals, small caps, and crude benchmarks. Capital crowding into a handful of growth names masks deteriorating breadth, eroding credit risk appetite, and a Treasury supply glut now colliding with waning Federal Reserve demand. The next directional impulse arrives with June US inflation prints. A hot surprise will harden the Federal Open Market Committee bias, lift short-end yields, bruise duration, and test the reflexive “own Nvidia, own Bitcoin” trade. A cool outcome would breathe life into the soft-landing consensus, crush implied volatility, and extend the AI-led melt-up.

Index Futures: Week Review and Structural Context

Monday, 7 July

Asia opened heavy after Washington delivered letters announcing tariff waves against 14 economies. Hang Seng fell 2.4 percent. Euro Stoxx 600 lost 0.9 percent as miners sold off on weaker China price data. US futures gapped lower, erasing roughly one-week’s progress. S&P 500 September contract printed 6 245 intraday, flirting with a break of the 50-day average for the first time since March. Nasdaq-100 held comparatively firm, drawing support from overnight chatter that two sovereign wealth funds bought blocks of Nvidia and Broadcom on Friday’s close.

Tuesday, 8 July

Dip buyers returned before the US cash open. Dealer gamma flipped positive once ESU25 reclaimed 6 280, forcing dealers to buy back hedges and fueling a reflexive 0.75 percent rebound. Nvidia added 3.1 percent, Amazon 2.4 percent, while Russell-2000 underperformed by 1.3 percent, reflecting small-cap sensitivity to tariff-driven margin compression. Treasury curve bear-flattened after a sloppy three-year note auction.

Wednesday, 9 July

A Bloomberg headline suggested the White House might “sequence” duties to soften the consumer shock. Equity bulls seized the nuance. Nasdaq-100 September ticked to a fresh contract record at 23 112. Tesla, freshly excluded from Canadian retaliatory measures, ripped 6.8 percent on above-consensus Q2 delivery whispers. VIX closed at 14.87, its lowest print since early May. Under the surface, SKW skew index jumped four points, hinting at stealthy crash-put demand.

Thursday, 10 July

The rally stalled. A 30-year Treasury reopening tailed 3.2 basis points with bid-to-cover of 2.17, weakest since October. Ten-year yield punched through 4.40 percent intraday before post-auction short covering trimmed the move. Growth stocks shrugged. Bank of America’s weekly Flow Show flagged a record $4.8 billion retail inflow into the AI ETF cohort. S&P 500 equal-weight lagged cap-weight by 1.7 percent on the week-to-date.

Friday, 11 July

Overnight, USTR escalated by floating 35 percent auto tariffs on Canada and reviving Section 301 tools against Mexico. European carmakers puked at the open. US futures bled points all session with no material bounce. ESU25 settled 6 300, down 0.36 percent from the prior Friday; NQU25 finished fractionally negative. Five-day advance-decline ratio for NYSE hit 0.73, lowest since February.

Structural Takeaways

Breadth decay persists. Only 27 percent of S&P names hold above their 50-day moving average.

Dealer gamma remains positive near-term but collapses beneath ESU25 6 230 and NQU25 22 600, leaving markets exposed to convexity squeeze on a downside breach.

Equity vol-rate correlation has flipped positive, a warning that bond-market turbulence can now propagate directly into equities rather than mute them.

Tariffs and the Macro-Political Overlay

The Trump administration spent the first half of 2025 preaching “ally-shoring” but pivoted hard in late June, invoking Cold War language around “strategic dependency.” The immediate catalyst was a Commerce Department review showing the US share of high-end semiconductor tooling imports from Japan and the Netherlands slipping from 71 percent in 2023 to 46 percent in Q1 2025 after new export permits slowed approvals. Beijing exploited the gap by subsidizing domestic champions and dumping mid-tier chips in Latin America at below cost.

Phase One Tariff Package

Consumer electronics: 30 percent duty on laptops, tablets, and certain handsets assembled in Vietnam, Mexico, and Malaysia.

Metals and rare-earth magnets: 25 percent across the board, with carve-outs for NATO suppliers.

Footwear and apparel: 25 percent if more than 55 percent of value added occurs outside the United States.

Cumulatively, the package lifts the average tariff rate from 11.4 percent to 18.7 percent, the highest since 1933. Yale Budget Lab’s dynamic general equilibrium model assigns a 0.8 percentage-point hit to 2025 real GDP, erasing roughly 578 000 jobs. Their price impact simulation adds 2 700 dollars to the median household goods basket, front-loaded into Q4 2025 as contracted imports clear customs.

Global Retaliation

Canada threatened 35 percent on US passenger vehicles and proposed a two-year moratorium on US dairy above its WTO quota.

EU signaled a proportional response on big-tech digital services revenue, along with a green-tech subsidy complaint at the WTO.

Mexico hinted at labor-intensive punitive tariffs spanning pork, soybeans, and light-duty trucks, weaponizing supply chains tied to swing-state electorates.

Historical Parallel

The 1930 Smoot-Hawley Act raised average duties to 19.3 percent. Within 24 months, global trade contracted by 40 percent in nominal terms. Today’s production networks are far deeper, and information flows instant. A finer-grained tariff regime may avoid Smoot-Hawley scale volume collapse, yet second-order effects on investment timing, working capital, and supply chain redundancy will erode productivity.

Artificial-Intelligence Mania(yes he said the M-word)

Market Share and Profit Pools

Seven listed US names: Nvidia, Microsoft, Amazon, Alphabet, Meta, Broadcom, AMD; now command 34 percent of S&P 500 market value, up from 23 percent one year ago. Their aggregate net income share sits at 21 percent. The remaining gap is pure future expectation. Sell-side analysts lifted 2025 Nvidia earnings estimates by 29 percent during Q2, the largest quarterly upward revision for any megacap since Apple in 2012.

Mechanisms Driving Exuberance

ETF flows: AI-branded ETFs pulled in $11.6 billion year-to-date, dwarfing renewable-energy flows by a factor of four. These vehicles allocate mechanically by market cap, reinforcing self-referential demand.

Vol-selling funds: Structured product desks write out-of-the-money calls against tech indexes to fund put purchases elsewhere, suppressing near-dated implied vol and drawing marginal buyers who misread low vol as low risk.

Retail social signals: TikTok has minted a new class of “GPU spec miners” posting rig unboxings, fueling the perception of inevitable upside. Google Trends for “Nvidia stock split” beat “Bitcoin halving” the week ending 27 June.

Valuation and Risk Flags

Price-to-sales: Nvidia trades 37x expected 2025 revenue, higher than Cisco’s dot-com peak.

Cash-flow margin: Nvidia gross margin at 78 percent sits 300 basis points above its prior cycle ceiling, unlikely to persist once new GPU entrants and in-house ASICs gain scale.

Capex super-cycle: Microsoft, Alphabet, Amazon will spend a combined $235 billion on datacenters this year, roughly equal to the entire 2022 US commercial real-estate construction outlay. Asset turns will lag two years, constraining free cash flow.

Strategic Conclusion

The AI trade is momentum-driven and reflexive, not price-discovery driven.

Participation remains under-hedged, making the complex vulnerable to exogenous funding shocks such as a Treasury auction failure or a surprise uptick in core inflation resetting the discount rate.

Sentiment and Positioning Cross-Currents

VIX prints sub-15 yet SKW shows persistent right-tail premium collapse and left-tail rise, a pattern typical ahead of regime shifts.

CBOE SPEX index of equity option flow reveals a fourth straight week where put notional exceeds call notional despite spot rallies. Institutions quietly pay for disaster insurance.

GS Prime net-notional long in tech sits at the 97th percentile of the past decade. Short alpha has collapsed as crowded shorts squeeze episodically.

Cross-asset volatility correlation flipped positive in June. Previously, higher bond vol compressed equity vol via diversification flows; now both rise in tandem, signaling macro contagion risk.

Federal Reserve and Treasury Supply

FOMC minutes acknowledged “lack of further progress” toward the 2 percent target. Core services ex-shelter cools, yet supercore indices sticky. Governor Waller floated a permanently larger but shorter-duration balance sheet, signaling the Fed may stop SOMA roll-offs at 6-year notes rather than the current 10-year cap. That reduces natural bid in long bonds even if runoff slows.

Treasury faces $2.27 trillion net issuance in fiscal 2025. Foreign official bids cover only 17 percent year-to-date, down from 24 percent in 2022. The June 30-year reopening tailed 3.2 basis points, worst since October. Bid-to-cover at 2.17 sits below the 5-year median of 2.31. A regime where dealers absorb more duration with thinner balance sheets magnifies auction slippage risk, feeding into term premium and equity discount rates.

Inflation Data Scenarios

Consensus: June headline CPI 2.6 percent, core 3.0 percent. PPI 2.8 percent.

Hot scenario: Headline 2.9 percent, core 3.2 percent. Fed swaps price out two cuts. Two-year yield targets 5.05 percent. ESU25 pierces 6230 triggering dealer negative gamma, air pocket to 6105. Bitcoin narrative pivots to inflation hedge, prints 122 000 but fades as real yields jump. WTI pops to 70 dollars on macro hedge demand, then stalls when dollar rockets.

Inline: Market stays range-bound. Soft-landing narrative endures. VIX sinks toward 14. AI complex resumes steady grind higher.

Cool: Headline 2.4 percent, core 2.8 percent. Fed cut probability for September jumps above 80 percent. Ten-year yield drops to 4.20 percent, curve bull-steepens. NQU25 screams through 23,300 into thin air. Bitcoin drifts but holds gains.

Tactical Plays

Short NQ below 22 800 targeting 22 600 with stop above 23 000.

Fade WTI 69 to 69.2 zone, cover 66 to 66.2, reverse long if spot closes above 70.6 on two-hour chart.

Buy Bitcoin dips to 112 to 114 thousand, stop below 110 thousand, target 125 thousand.

Long Bitcoin versus short NQ one-for-one, seeking 15 to 20 percent relative outperformance, cut if ratio underperforms 7 percent.

Steepener via five-thirty Treasury futures, stop on flattening beyond 8 basis points.

WEEKLY LEVELS:

Subscribers are urged to use the tradingview indicator to plot the levels.

NOTE: SUBSCRIBERS ARE URGED TO JOIN THE DISCORD AT THEIR EARLIEST CONVENIENCE.

Discord link here: