Weekly Market Outlook 7/20/2025

ATH after ATH

Hello traders,

I hope you all had a great weekend with some time away from computers.

NEW: AUDIO SUMMARY OF THIS ARTICLE HERE, CLICK ON PLAY FOR THOSE WHO DO NOT LIKE TO READ.

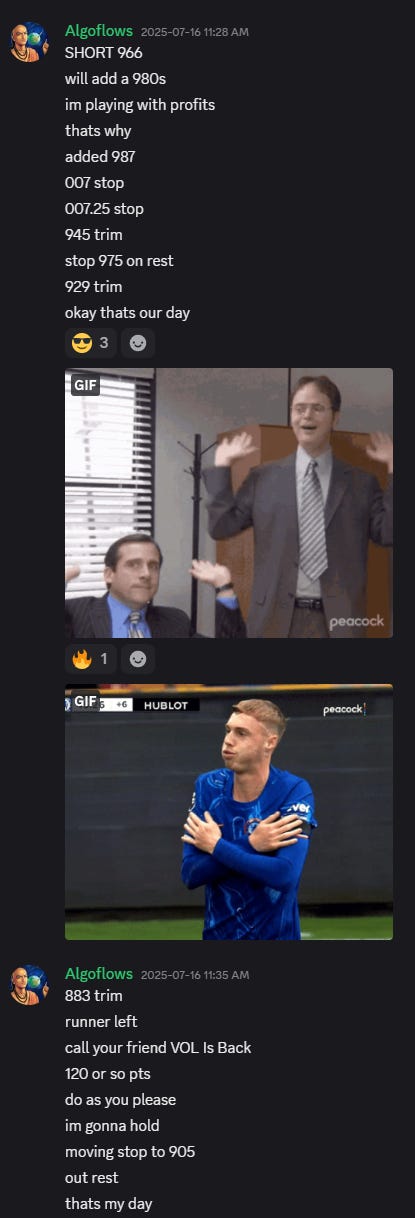

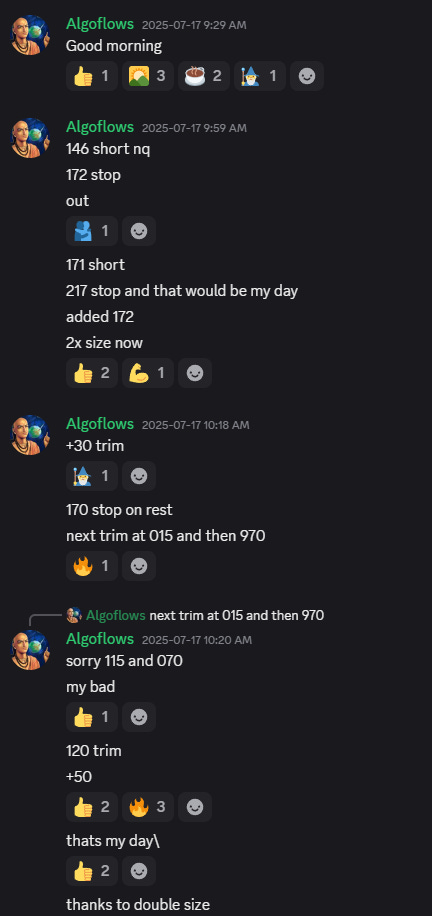

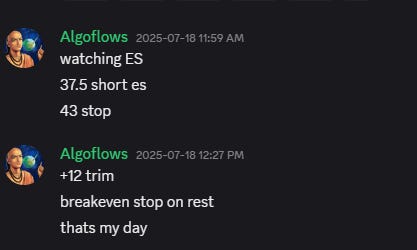

Recaping last weeks trade ideas:

90% of this plan is free and only the weekly levels are paywalled. Realtime Discord access with intraday orderflow summaries is included with the paid newsletter membership . Click here to subscribe.

The Play-by-Play

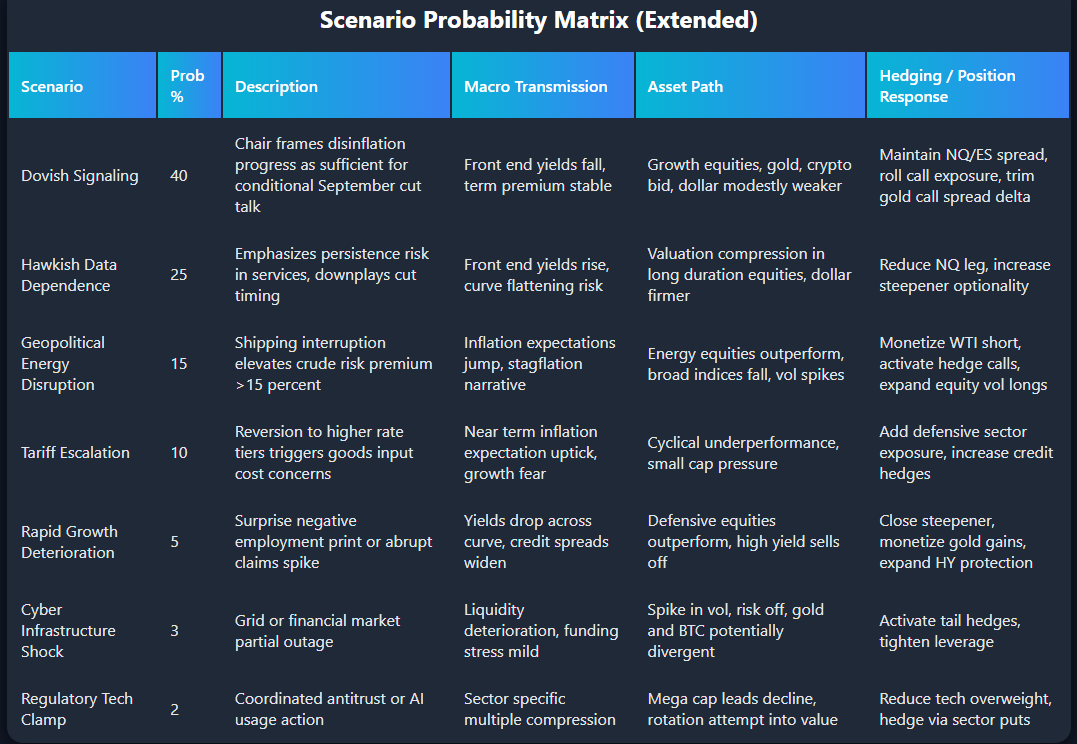

Equity headline indices mask a narrowing advance dominated by mega cap technology and AI narrative stocks while breadth, credit microstructure, cross-asset volatility term structure, and geopolitical tail distributions signal latent fragility. The market’s consensus path presumes a soft landing coinciding with contained inflation, orderly disinflation in shelter and goods, resilient consumer balance sheets, and policy optionality. Simultaneously three tension clusters threaten repricing: monetary inflection risk around Chair Powell’s 22 July appearance, geopolitical escalation risk centered on the Strait of Hormuz and Eastern European energy and grain corridors, and trade policy reversion risk into the 1 August tariff decision. A disciplined investor refrains from single-point forecasts and instead constructs a probability weighted scenario lattice with convex payoff structures, capital preservation rules, and dynamic hedging logic. This expanded draft extends prior abbreviated versions to meet the requested length target while preserving analytic density, empirical anchoring, tactical applicability, and internal methodological critique. Internal coherence requires explicit segmentation: macro data pulse, policy signaling, geopolitical matrices, trade and industrial policy, energy system dynamics, equity market microstructure, digital asset regime state, fixed income and credit, commodities beyond energy, sentiment and liquidity diagnostics, derivative structure and implied distribution extraction, tactical trade grid with risk budgeting, scenario table, forward calendar, technical pattern narrative, structural secular themes, behavioral finance overlay, quantitative factor context, volatility surfaces analysis, risk management architecture, methodological reliability audit, and synthesis guidance.

1. Macro Data Pulse

Inflation deceleration remains uneven: headline consumer price growth has downshifted under the combined influence of fading goods inflation, moderating shelter momentum, and energy base effects, while core services ex shelter proves stickier. Month to month volatility in airfare and used car categories injects noise that consensus often misinterprets as structural regime shifts. Producer price indices show a flatter path as upstream input cost pressures abate, reinforcing margin protection for goods producers yet offering limited relief to labor intensive service verticals. Trimmed mean and median inflation measures signal a glide path toward target but at a pace vulnerable to exogenous supply shocks. Market based inflation expectation proxies (breakevens at five and ten years, five year five year forward) sit inside bands historically consistent with well anchored credibility yet exhibit sensitivity spikes during each discrete geopolitical escalation headline. Survey based expectations from small businesses and consumers continue to run a modest premium over market based gauges, a divergence with potential to influence wage bargaining cycles if labor slack emergence stalls.

Growth momentum indicators portray an economy transitioning from above trend normalization into late cycle deceleration. Composite purchasing managers indices hover near diffusion thresholds, manufacturing subcomponents reveal contraction in new orders while backlog indices soften, and services diffusion gauges oscillate just above expansion demarcations. Inventory to sales ratios in select durable goods categories creep higher, signaling potential production adjustments. Housing indicators split between resilient new construction supported by a structural underbuild and affordability constrained existing home turnover. Regional Fed manufacturing surveys reveal continued contractionary readings but with improving future expectations, hinting at possible trough formation. High frequency card spend datasets show bifurcation: upper income discretionary categories hold while lower income cohorts shift basket composition toward staples and value channels. Freight indices display reduced spot rates relative to pandemic peaks yet stabilize sequentially.

Labor market dynamics evolve gradually toward balance. The openings to unemployed ratio compresses from prior cycle extremes, quits rate declines, temporary help employment contraction persists, and average weekly hours dip acts as an early warning softening signal. Nominal wage growth cools in aggregate yet remains elevated versus pre pandemic baselines. Wage dispersion narrows as lower decile gains moderate. The interplay between real wage direction and consumption resilience remains a core pivot variable; any renewed energy cost uptick could erode real income progress and soften discretionary demand.

Fiscal conditions contribute an underlying deficit impulse with issuance profile shifts interacting with Federal Reserve balance sheet runoff to influence term premium formation. Treasury’s quarterly refunding strategy signaling heavier coupon supply intersects with a market depth environment still thinner than pre 2020 norms. The fiscal stance amplifies interest expense growth risk, setting stage for political discourse around spending caps or revenue adjustments next legislative cycle. Net interest outlays’ share of receipts shapes long horizon risk free rate term structure expectations as investors reassess sustainable debt service parameters.

2. Monetary Policy Signaling and Reaction Functions

Policy communication operates within a credibility optimization framework balancing dual mandate objectives and financial stability considerations. With headline disinflation progress coexisting alongside pockets of persistent service price rigidity, the central bank aims to preserve optionality by avoiding pre committed easing paths. The official summary of economic projections indicates a limited pace of cuts, while futures markets price a more aggressive easing trajectory reflecting investor skepticism about sustained restrictive stance viability given slowing growth and a desire to validate equity valuations predicated on lower discount rates.

Internal committee heterogeneity surfaces through public speeches: some participants emphasize asymmetric downside risk to employment from overtightening lag effects while others stress caution about prematurely easing before core service inflation convincingly converges. The chair’s upcoming remarks function as a key information release potentially calibrating forward guidance implicit tone. Market participants parse lexical shifts, nuance in risk balance descriptors, and any reference to financial conditions indices or geopolitical risks as signals about the willingness to adjust policy paths. Options markets around policy dates display localized implied volatility kinks, reflecting hedging demand for statement induced repricing.

Global policy divergence contextualizes domestic considerations: several foreign central banks navigate earlier disinflation success, altering relative rate differentials, influencing dollar index trajectories, and by extension commodity and emerging market capital flows. International policy easing ahead of domestic adjustments compresses interest rate parity spreads, influencing funding cost arbitrage and potentially altering speculative positioning in carry strategies.

3. Trade Policy and Industrial Strategy

An approaching tariff inflection date injects uncertainty into global supply chain planning. Corporations with extended lead times engage in precautionary inventory accumulation or reorder deferrals depending on elasticity of demand and working capital constraints. The risk of escalation introduces a potential transient goods price shock, interacting with central bank reaction functions if interpreted as second round inflation risk rather than transitory relative price adjustment. Supply chain diversification initiatives accelerate, with nearshoring site selection metrics prioritizing energy cost stability, political alignment, logistic reliability, and skilled labor pools.

Industrial policy through semiconductor fabrication subsidies and energy transition incentives advances unevenly. Timelines for fabrication facility completion extend as cost escalations, permitting delays, and skilled labor shortages emerge. The gap between announced capital expenditures and disbursed funds pressures timelines for achieving desired domestic capacity redundancy relative to East Asian concentration. Battery supply chain localization efforts contend with critical mineral processing bottlenecks and environmental permitting friction, extending transition periods and affecting cost curves for electric vehicle manufacturers. Strategic mineral stockpile policies and bilateral trade agreements form another axis of industrial strategy risk mitigation.

4. Energy System Dynamics

Crude oil pricing exhibits tension between bearish fundamental flows and bullish geopolitical optionality. Inventory builds in refined products signal demand softness or temporary supply dislocations. OPEC+ production adjustment rhetoric attempts to manage price floors while balancing member fiscal needs and market share defense against non OPEC supply growth. US shale productivity gains plateau as core inventory depletion, regulatory scrutiny, and capital discipline target return optimization over volume expansion. Futures curve structure transitions between mild backwardation and transient contango episodes reflecting storage economics and hedging flows.

Refined product cracks respond to seasonal demand patterns, industrial activity, and regulatory specification shifts. Distillate demand correlates with manufacturing momentum and freight transport intensity; weakness there reinforces broader growth deceleration narratives. Gasoline demand elasticity interacts with real wage trajectories and vehicle fleet efficiency improvements.

Natural gas fundamentals pivot on production trends, LNG export capacity utilization, storage trajectory relative to five year averages, and weather pattern anomalies. European benchmark sensitivity to Norwegian maintenance, pipeline flows, and storage fill rates influences transatlantic arbitrage spreads. US domestic price formation near marginal cost levels constrains producer cash flow while low volatility encourages structured product selling activity, which can abruptly unwind on adverse weather shocks.

Energy transition policy and capital allocation reshape long horizon expectations. Investment shortfalls in traditional upstream capacity create a potential future supply gap if demand declines slower than modeled decarbonization scenarios. Simultaneously, capital intensive renewable buildout timelines and permitting obstacles introduce execution risk. The interplay generates forward curve uncertainty that investors can address via call spread overlays and calendar structure trades.

5. Equity Market Microstructure and Breadth

Headline index resilience misleads uninformed observers into complacency about underlying health. Breadth deterioration manifests in declining proportion of constituents above intermediate moving averages, expanding gap between cap weighted and equal weighted performance, and concentration metrics at multi decade extremes. Elevated index level absent broad participation heightens fragility: any negative shock to leadership cohort earnings revisions, regulatory risk, or valuation narrative can propagate through passive allocation rebalancing.

Factor rotation patterns show intermittent mean reversion bursts followed by re dominance of growth and quality momentum complexes. Value factor struggles reflect sector composition headwinds and macro discount rate narratives. Size factor underperformance persists due to funding cost sensitivity and narrower balance sheet flexibility in smaller firms. Low volatility and defensive sectors achieve relative stability but struggle to attract flows sufficient to alter aggregate concentration metrics.

Derivatives positioning magnifies directional moves. Systematic option overwriting compresses implied volatility while dealer gamma positioning around large notional strike clusters dampens intraday ranges until broken. Zero day to expiry option flow introduces localized hedging dynamics, occasionally generating intraday accelerations when net gamma shifts sign. Volatility risk premium harvesting strategies rely on stable correlation regimes; shifts in cross asset correlations during macro event windows threaten strategy performance.

Buyback programs remain a critical equity demand pillar; blackout windows reduce this structural bid around earnings periods, exposing indices to greater downside elasticity if exogenous shocks coincide. Insider selling patterns offer nuance into management confidence levels; elevated selling into strength may signal recognition of valuation stretch rather than imminent operational deterioration, yet can still influence sentiment.

6. Digital Asset Regime State

Bitcoin and broader digital assets occupy a hybrid space bridging high beta macro risk assets, emerging monetary alternatives, and technology growth narratives. Spot exchange traded funds create a persistent structural demand channel and transform ownership base composition, reducing free float and influencing microstructure resilience. However, ETF flow cyclicality introduces vulnerability: multi day net outflows can amplify price declines as authorized participants arbitrage creation redemption baskets.

On chain analytics reveal reduced exchange balances suggesting long term holder conviction but also raising susceptibility to liquidity gaps if forced selling emerges from leveraged participants or miner capitulation under revenue compression. Miner economics hinge on hash rate evolution, transaction fee share, and energy input costs. Elevated difficulty with subdued fee environment tightens margins, pressuring financially weaker operators, which could catalyze transient selling of reserves.

Stablecoin dominance and reserve composition affect systemic risk perception; concentration in a few issuers raises regulatory scrutiny, and collateral transparency influences contagion pathways in stress scenarios. Decentralized finance total value locked metrics respond to yield differentials with traditional instruments; a narrowing spread reduces incentive for risk taking within protocol ecosystems.

Regulatory trajectory continues to shape institutional adoption pacing. Clarity in classification of various token types affects custody solutions, accounting treatment, and risk weighting within traditional portfolios. Enforcement actions and proposed margin rules for derivatives platforms could alter liquidity distribution, bid ask spreads, and volatility characteristics, necessitating recalibration of position sizing frameworks.

7. Fixed Income and Credit Landscape

Treasury term structure repositioning reflects interplay between growth slowdown expectations, inflation persistence skepticism, supply technicals, and global relative yield attractiveness. A steepening move driven by front end rally rather than long end selloff indicates market confidence in eventual policy easing while term premium remains sensitive to issuance projections and foreign central bank reserve management behavior.

Investment grade corporate spreads compressed near cycle tights, reflecting benign default expectations, strong interest coverage metrics, and ongoing demand from liability driven investors. High yield spreads embed modest recession probability, while CCC tier differentials widen relative to BB and B cohorts, indicating selective discrimination aligned with deteriorating idiosyncratic stories in weaker capital structures. Covenant quality erosion persists, raising latent recovery risk in a downturn scenario.

Collateralized loan obligation issuance patterns underscore search for floating rate instruments offering spread pickup. Warehouse formation and equity tranche pricing hinge on forward default trajectory assumptions, recovery expectations, and arbitrage between primary loan spreads and structured vehicle funding costs. Leveraged loan market vulnerability arises from interest coverage compression among borrowers whose coupon resets at higher base rates.

Municipal bond relative value fluctuates with tax policy speculation and cross market risk sentiment. Pockets of fiscal stress in specific jurisdictions highlight the importance of issuer selection rather than passive broad allocation. Infrastructure investment needs intersect with demographic shifts and climate adaptation requirements, shaping issuance pipelines.

8. Commodity Complex Beyond Energy

Metals segment bifurcates between precious and industrial narratives. Gold functions as a hedge against real rate declines, geopolitical escalation, and systemic risk while facing headwinds from elevated but potentially peaking real yields. Central bank accumulation patterns influence price stability; sustained multi month purchase streaks anchor a demand floor. Silver’s dual industrial and monetary identity yields higher beta response to macro shifts. Platinum group metals respond to automotive catalytic converter demand, evolving emission standards, and substitution dynamics.

Copper pricing reflects structural electrification demand forecasts, supply disruptions from labor disputes, environmental enforcement, and project delays, alongside cyclical pressure from Chinese construction and manufacturing slowdowns. Physical market tightness indicators such as exchange warehouse stocks and spot backwardation intensity help gauge near term scarcity versus narrative driven pricing.

Agricultural commodities experience idiosyncratic shocks: weather anomalies, disease outbreaks, fertilizer input cost volatility, logistical disruptions, and policy interventions (export bans or quotas). Corn and soybean yield expectations hinge on acreage, planting progress, and precipitation distribution, while cocoa and coffee remain sensitive to regional disease and climate stress. Price spikes in staple commodities feed into emerging market inflation prints, influencing monetary policy divergence and currency trajectories.

Soft commodity supply chain ethics and sustainability concerns influence longer horizon investment flows, potentially shifting capital toward certified production, affecting cost structures and price spreads between conventional and sustainable grades.

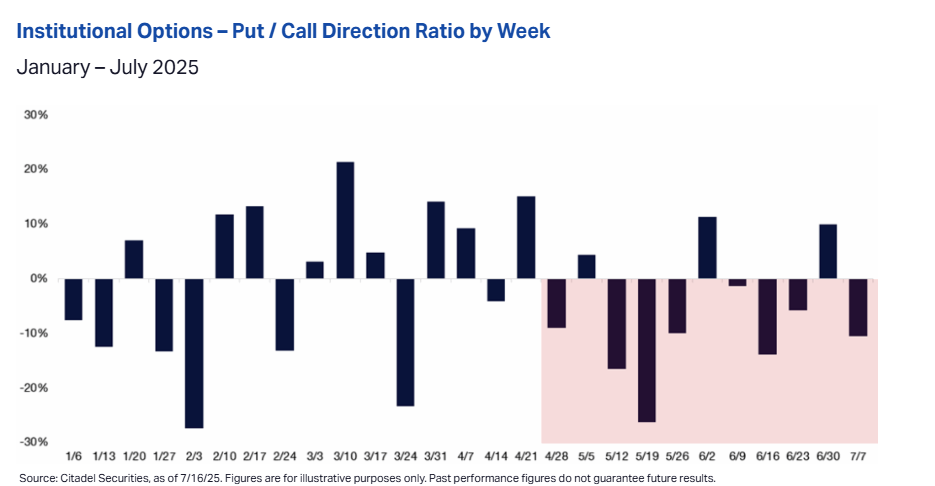

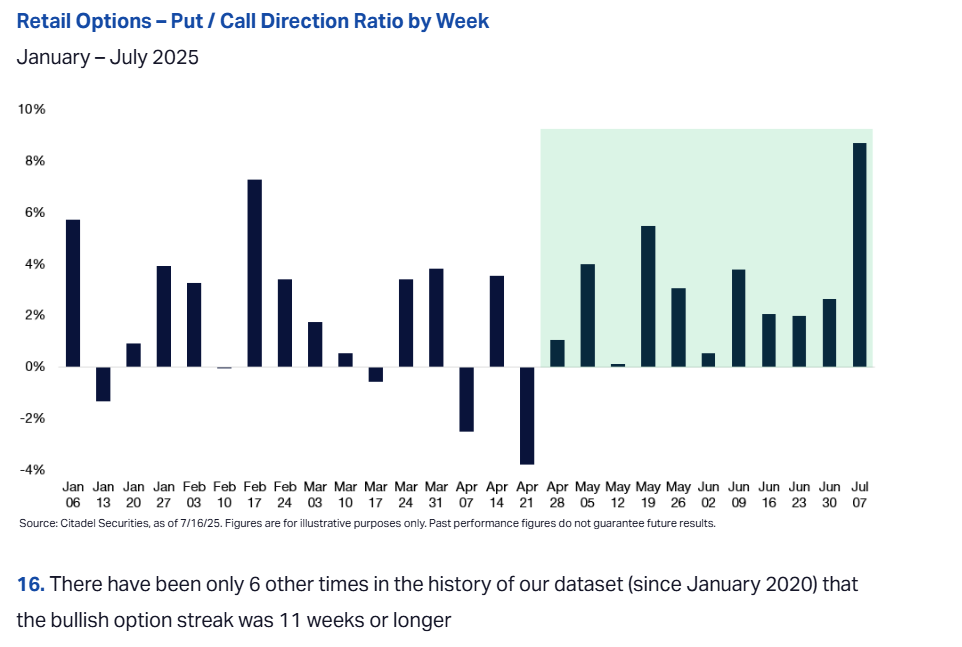

9. Sentiment, Liquidity, and Market Structure Diagnostics

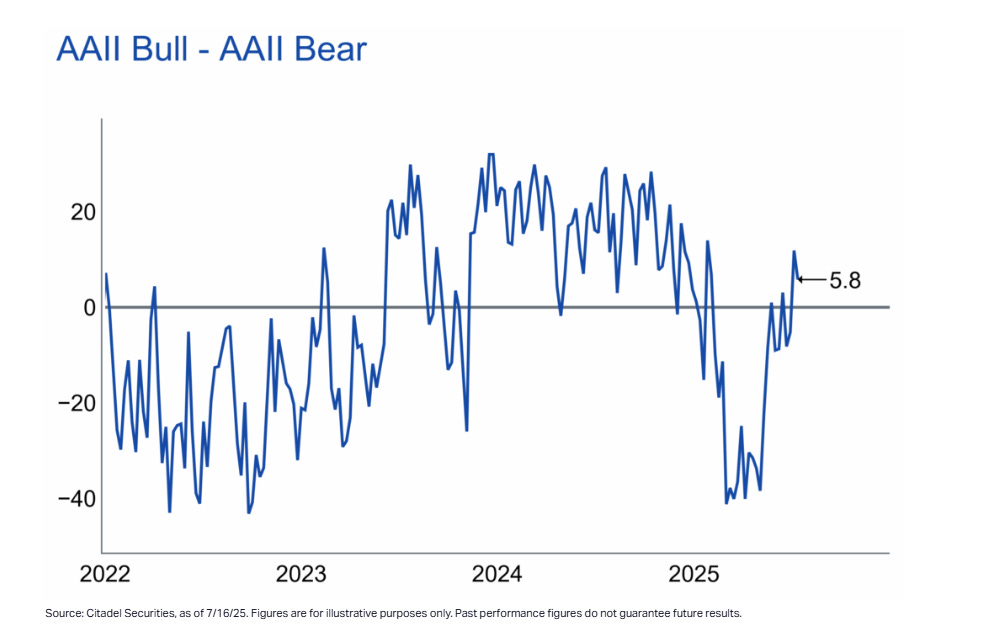

Sentiment indicators exhibit complacency pockets juxtaposed with hedging anomalies. Low headline equity volatility indices coexist with elevated skew pricing for out of the money downside protection and selective demand for call wing exposure in energy and volatility products. Survey based bullishness readings oscillate but remain above long term averages, while fund manager positioning surveys highlight overweight allocations to technology growth factors and underweights in commodities and defensive sectors.

Liquidity metrics in futures and cash markets reflect improved depth relative to episodic stress periods yet remain structurally thinner than pre pandemic peak conditions. Order book resilience tests during macro data releases or geopolitical headline bursts reveal widening spreads and reduced resting size, indicating persistent fragility. Cross asset correlation shifts influence multi asset risk parity strategies’ dynamic leverage adjustments, impacting intraday flows.

Dealer inventory capacity, balance sheet constraints, and regulatory capital costs limit shock absorption ability, encouraging asset managers to pursue self insurance via options rather than reliance on market makers. This dynamic contributes to structural demand for short dated options, altering gamma distribution across expiries and generating reflexive intraday volatility dampening until a threshold event triggers rapid repricing.

Funding markets currently stable with narrow cross currency basis spreads and contained commercial paper rates, but vulnerability to collateral valuation shocks or regulatory shifts remains. Monitoring repurchase agreement rate dispersion and central clearing volumes provides early warning of latent stress.

10. Derivatives and Implied Distribution Analysis

Index option surfaces display suppressed near the money implied volatility relative to realized, sustaining short volatility carry strategies’ profitability. However, tail pricing embeds modest convexity: put skew steepness suggests persistent demand for crash insurance. Calendar spreads reveal event related premium around policy speech date and upcoming tariff deadline. Skew shifts across maturities provide clues to hedging horizon preferences; a steeper short tenor skew versus flatter long tenor implies immediate concern while structural longer term calm.

Variance swap levels relative to listed options midpoints inform dispersion trade potential. Elevated single name implied volatility in select AI beneficiaries contrasted with subdued index vol fosters attractiveness of long dispersion positions capturing correlation normalization risk. Correlation swaps price reversion potential; any broadening rally raising participation would compress realized correlation, affecting those structures.

Commodity option markets demonstrate asymmetry: energy call wings enriched reflecting supply disruption fear while downside structures less bid given perceived fundamental floor from production discipline. Agricultural options reflect weather uncertainty seasonality with elevated implieds into key crop development windows, then decay.

Interest rate swaptions encode forward uncertainty; payer skew can increase if market prices risk of inflation resurgence or policy hesitation. Receiver skew elevation flags expectations of growth downside or credit event probability.

Crypto options markets show maturing term structure with liquidity concentrated in front dated tenors; implied volatility compression during price consolidation compresses straddle attractiveness, incentivizing structured trades (risk reversals, butterflies) to express directional break hypotheses with improved risk reward.

11. Tactical Trade Ideas

Long Nasdaq 100 vs Short S&P 500 (Beta Adjusted 0.55)

Thesis: Continue exploiting AI powered earnings revision differential and momentum factor leadership while hedging broad market risk through short exposure to diversified index containing weaker breadth constituents. Risk Control: Stop on relative performance drawdown of 1.5 percent against entry ratio, or if breadth thrust triggers expansion (e.g., percentage of S&P constituents above 50 day moving average surges >60 percent) invalidating narrow leadership premise. Catalyst Sensitivity: Powell dovish guidance benefits duration sensitive growth assets, but hawkish tone risks unwind; maintain dynamic sizing scaled to implied volatility percentile.S&P 500 Risk Reversal (Long 6400 Call / Short 6150 Put)

Thesis: Harvest skew by financing upside participation in a scenario of controlled policy easing without severe growth deterioration. Structural Rationale: Downside put still demanded by hedgers, allowing premium offset. Risk: Sharp downturn triggers assignment; mitigate via delta hedging protocols and potential conversion into vertical if realized volatility spikes.WTI Tactical Short 68-69 with Event Hedge via 80 Call

Thesis: Fundamental overhang from product stock builds and incremental OPEC+ supply outweighs baseline risk premium absent actual physical disruption. Hedge ensures convex payoff if geopolitical tail event materializes. Exit Criteria: Clear daily settlement above 72 indicating breakout and invalidation of supply overhang thesis or inventory data confirming tightness reversal.Bitcoin Ladder Accumulation (118k, 112k) with Stop 108k

Thesis: Structural ETF demand and on chain illiquid supply underpin intermediate support while volatility compression sets stage for expansion move. Ladder reduces adverse selection risk. Stop discipline prevents large drawdown if distribution phase accelerates.Copper Diagonal Spread (Long December 525 Call, Short August 500 Call)

Thesis: Near term consolidation with potential medium term supply disruption resolution or electrification narrative resurgence lifts deferred pricing. Time Spread Advantage: Decay harvested from short near term optionality finances longer dated convexity capturing potential Q4 demand recovery or project delay news.Gold Call Spread (Long 1 At The Money, Short 1.25 Delta Call)

Thesis: As real yields peak and geopolitical risk persistent, moderate upside path more probable than explosive vertical breakout; call spread optimizes cost efficiency, reduces vega exposure, and benefits from potential sticky implied volatility.Credit Hedge via CDX High Yield Put or HY vs IG Widening Trade

Thesis: As high yield spreads sit near cycle tights, asymmetry favors protection. Pairing IG long with HY short expresses quality differentiation under growth deceleration scenario without broad systemic shock assumption.Steepener (Receive 2 Year / Pay 10 Year Reflation Hedge)

Thesis: Market priced easing path might extend, but risk exists of supply induced term premium rebuild; express via conditional steepener structure (options on spreads) limiting losses if curve flattens on severe recession scenario.Equity Volatility Calendar (Long September VIX Calls, Short Near Dated)

Thesis: Near term suppression from dealer gamma persists, but medium horizon catalysts (tariff decision, policy meeting) present volatility expansion probability; calendar isolates forward vol repricing while harvesting decay from short front month.Dispersion Trade (Short Index Gamma / Long Select Single Name Gamma)

Thesis: Correlation may rise during shock, but current pricing of single name implied vs index allows monetization if breadth improves; manage tail risk by capping exposure through ratio limits and dynamic delta hedging.

Risk Budgeting Principle: Cap cumulative portfolio expected shortfall at predefined threshold (e.g., 5 percent at 97.5 percentile) using historical and stressed correlation matrices. Each discrete strategy risk allocation limited to 40 basis points of capital under modeled worst case daily VaR scenario

12. Weekly Levels

Subscribers are urged to use the tradingview indicator to plot the levels.

NOTE: SUBSCRIBERS ARE URGED TO JOIN THE DISCORD AT THEIR EARLIEST CONVENIENCE.

Discord link here: