Weekly Market Outlook 8/24/2025

PIVOT! PIVOT! PIVOT!

Hello traders,

Hope you all had a great weekend and some much needed time away from screens.

You can jump to the Weekly levels by clicking on them directly.

AUDIO SUMMARY OF THIS ARTICLE HERE

But first, a brief recap of last week’s ideas.

AlgoFlows’s Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Realtime Discord access with intraday orderflow & option dealer summaries included with the paid newsletter membership . Click here to subscribe.

The Week in Review: A Tale of Two Markets

The past week on Wall Street was a study in contrasts, a dramatic narrative that saw markets plunge toward a technical precipice before being rescued by a powerful, policy-driven reversal. The trading week began under a cloud of persistent selling pressure, with sentiment soured by inflation fears, a faltering technology sector, and signs of a weary consumer. By Thursday's close, the S&P 500 index had posted its first five-session losing streak since January, a worrying development that suggested the summer rally was losing steam. However, the entire complexion of the market changed in a single session on Friday, as a pivotal speech from Federal Reserve Chairman Jerome Powell at the annual Jackson Hole economic symposium provided a "stick save" that sent risk assets soaring and turned a week of losses into modest gains for the major indices.

My first thoughts were that Powell was actually Hawkish and not Dovish.

Upon further reflection and after rewatching the entire statement I think Powell was very slightly Hawkish and that means we will continue our regular programming of Uponly.exe

The initial weakness was pervasive and led by the very names that had propelled the market to record highs. The technology sector, in particular, hit a significant "pothole," with the Nasdaq Composite logging declines in six of the last seven sessions heading into Friday. The pain was concentrated in the MegaCap stalwarts that have defined the market's advance; Nvidia (NVDA), Advanced Micro Devices (AMD), Palantir (PLTR), and Meta Platforms (META) were all down more than 5% at one point during the week. This sell-off was fueled by a combination of factors, including simple profit-taking after a historic run, alongside more concrete concerns. The Trump administration's floating of new tariffs on imported semiconductors rattled an industry reliant on global supply chains, while persistent inflation data stoked fears that the Federal Reserve would be forced to keep interest rates "higher for longer".

This anxiety was compounded by a drumbeat of concerning economic signals. Inflationary pressures, which had seemed to be moderating, showed renewed signs of life in data from the Philadelphia Fed Index and the S&P Global PMI. This came on the heels of the prior week's shockingly hot Producer Price Index (PPI) report, which suggested that cost pressures were building aggressively within the corporate supply chain. Simultaneously, the American consumer, the bedrock of the U.S. economy, began to show signs of strain. Disappointing earnings reports and cautious outlooks from major retailers, including Walmart (WMT), BJ's Wholesale Club (BJ), and Target (TGT), raised alarms about the durability of consumer spending in an environment of elevated borrowing costs and rising prices for essential goods.

Just as the bearish narrative seemed to be taking hold, the market executed a stunning about-face on Friday, August 22nd. The catalyst was singular and powerful: Chairman Powell's address from Jackson Hole, Wyoming. In his remarks, Powell laid the groundwork for a potential interest rate cut at the Federal Reserve's upcoming September meeting, a dovish pivot that investors had been desperately hoping for.

He explicitly acknowledged the rising downside risks to the labor market, a key shift in tone that signaled the central bank's focus may be moving from fighting inflation to preemptively supporting economic growth.

For the first time with such directness, Powell confronted the economic realities of the administration's aggressive trade and immigration policies. He stated plainly that "significantly higher tariffs across our trading partners are remaking the global trading system" and acknowledged that the pass-through effects on consumer prices are "now clearly visible". This was a direct validation of recent data showing a surge in producer prices and an admission that trade policy is now a primary variable in the Fed's inflation equation. He also noted that "tighter immigration policy has led to an abrupt slowdown in labor force growth," a key structural change impacting the supply side of the labor market.

However, the crucial element for markets was how Powell chose to frame these inflationary pressures. Rather than signaling alarm, he characterized the price increases stemming from tariffs as a likely "one-time shift in the price level". This framing is critical, as it suggests the Fed is prepared to "look through" the immediate impact of tariffs on the inflation data, viewing it as a temporary shock rather than the beginning of a persistent, wage-driven inflationary spiral. This interpretation gives the central bank the necessary policy flexibility to focus on what it now appears to view as the more pressing risk: a potential deterioration in the labor market.

The dovish tilt of the speech was anchored firmly in Powell's detailed commentary on employment. He described the current labor market as being in a "curious kind of balance," one that results from a marked slowing in both the supply of workers, driven by new immigration policies, and the demand for workers from employers. He warned that this "unusual situation suggests that downside risks to employment are rising" and, critically, that if these risks materialize, "they can do so quickly in the form of sharply higher layoffs and rising unemployment". This forward-looking concern about a rapid, nonlinear break in the jobs market was the clearest signal of the Fed's shifting priorities.

The culmination of these points was a clear, albeit carefully worded, policy signal. Powell concluded that with the Fed's policy rate now 100 basis points lower than it was a year ago, the central bank has the latitude to "proceed carefully as we consider changes to our policy stance". This was universally interpreted by investors as opening the door wide for an interest rate cut at the Federal Open Market Committee (FOMC) meeting in September, unleashing a wave of buying across risk assets.

Powell's speech represents a calculated and significant policy gamble. The Federal Reserve is now explicitly signaling a willingness to tolerate a period of visibly higher, tariff-induced inflation, a known and quantifiable risk: in order to preemptively insure against a potential, but not yet realized, sharp downturn in the labor market. This marks a strategic shift away from the purely data-dependent, inflation-fighting posture of the past two years toward a more forward-looking, risk-management approach that prioritizes the employment side of its dual mandate. The Fed is fully aware of the inflationary impulse building in the economy; Powell's own words confirm that the effects of tariffs are "clearly visible" and will "accumulate over coming months," a fact corroborated by the recent 3.3% year-over-year jump in the Producer Price Index. Despite this clear and present inflation pressure, the entire thrust of his forward guidance was on the potential for a labor market shock. By choosing to emphasize a hypothetical future risk (rising unemployment) over an actual current risk (rising inflation), the Fed is making a deliberate policy choice. It is accepting higher inflation in the near term as the cost of preventing a recession. This recalibrates the market's understanding of the central bank's reaction function. The bar for a hawkish response to hot inflation data is now considerably higher, while the bar for a dovish response to any signs of weakness in employment data is now much lower. This logic fully justifies the market's explosive "risk-on" reaction and validates the return of the "Powell put," though its strike price now appears to be tied more directly to the unemployment rate than to stock market volatility.

The S&P 500 Equal Weight Index (SPXEW), which gives the same influence to every company in the index regardless of size, surged to a new all-time high. The Russell 2000 (RUT), an index of small-cap stocks, rocketed higher by over 3.8% on Friday alone. This broadening of participation was a healthy sign, indicating that investor confidence was spreading beyond the handful of MegaCap technology firms. By the closing bell, the S&P 500 (SPX) had clawed back all its weekly losses to finish modestly higher by approximately 0.30%, closing near 6,469, while the Dow Jones Industrial Average set a new record high.

Index Futures: Tech Stumbles, Value Broadens

The week's sharp swings were on full display in equity index futures, where early weakness reversed into a strong rally. The split between the broad S&P 500 and the tech-heavy Nasdaq-100 highlighted leadership rotation and a possible broadening of the market advance.

S&P 500 E-mini (ES) Analysis

The front-month S&P 500 E-mini contract (September 2025: ESU5) was volatile. After five straight down sessions into Thursday, the contract rebounded sharply Friday, closing the week up about 1.51% at 6484.75.

Technical action confirmed key support. The index dipped to test its 20-day moving average near 6381, which has acted as a floor since summer. Buyers stepped in aggressively near 6360–6350, confirming the short-term uptrend.

Talk of a bearish double top emerged after peaks near 6500 on August 15 and 21. The rejection on the 21st gave credibility to this view, with neckline support flagged near 6370–6375. A break there would have implied deeper downside. Powell’s speech negated that case. The ES closed back above the weekly pivot of 6404 and just shy of the prior week’s 6481 high. A move above that level would invalidate the double top and open the way toward resistance near 6524.

The strongest bullish sign is broadening participation. The breakout in the S&P 500 Equal Weight Index (SPXEW) confirmed the rally is expanding beyond the “Magnificent 7” into the broader market. This signals healthier breadth and a more durable advance.

Nasdaq-100 E-mini (NQ) Analysis

The Nasdaq-100 E-mini (September 2025: NQU5) lagged most of the week, pressured by tech-specific risks. It joined Friday’s rally, ending up 1.56% at 23582.75, but its earlier weakness stood out.

The index was hit by reports that Nvidia told suppliers to halt production of its H20 AI chip for China. Concerns about demand combined with profit-taking in a stretched sector. Technicals show consolidation between support near 23,750 and resistance near 23,950, with supply overhead at 24,050. Key support emerged at 23,000, and a break there could trigger a fall to 22,500–22,800.

Bulls hold the edge as long as price stays above 23,600–23,800. The market has rewarded dip buyers since April, with Friday repeating that pattern. For bears, only a decisive high-volume break under 23,000 would shift control. For now, the dovish tone from Jackson Hole reinforced support.

Actionable Trade Ideas

ES (Bullish Continuation): The reversal Friday and broadening breadth favor higher levels. A pullback toward 6440–6450 could offer long entry. Targets: retest of 6500, then 6525. Stop: below pivot 6404. Thesis: Powell’s dovish stance erased bearish patterns and rotation into value supports upside.

NQ (Relative Value Short/Pairs Trade): For those skeptical of tech, a long ES / short NQ pairs trade benefits if leadership rotates away from MegaCap tech. Alternatively, a tactical NQ short near 24,000–24,050 supply could target 23,600 if rejection signals appear. Thesis: sector-specific risks and valuations set Nasdaq up to underperform.

Bond Market: Yields, Auctions, Curve

Equity optimism contrasted with bond caution. Fed policy, inflation, and heavy issuance created strain.

The 10-year yield ended near 4.31% after volatile trading. The curve steepened as long yields rose faster than short ones. Short-term rates stay anchored by Fed policy, while heavy supply and inflation fears push long yields higher.

Treasury auctions revealed mixed demand.

The August 15 sale of 10-year notes priced at 4.255% and showed solid participation from indirect and direct bidders, leaving dealers with less supply. Positive signal.

The August 7 sale of 30-year bonds was weak. Bid-to-cover ratio 2.27, bonds sold at 4.813%, above pre-auction levels.

The 20-year auction was also soft, bid-to-cover 2.46, with a tail above when-issued pricing.

Short-term bill sales continued to clear at yields above 4%, in line with Fed policy.

Inflation's Tug-of-War: CPI vs PPI

Two July inflation reports sent conflicting signals. CPI eased, PPI surged. The contrast showed consumer prices holding steady while producer prices reflected tariff-driven cost pressure.

Consumer Price Index (CPI) – July 2025

Released August 12. Headline CPI rose 0.2% m/m and 2.7% y/y, below the 2.8% forecast. This cooled rate cut anxiety. Core CPI rose 0.3% m/m and 3.1% y/y, still sticky. Services drove inflation, led by shelter up 3.7% y/y. Gasoline down 9.5% y/y held the headline down. Services ex-energy rose 3.6%.

Producer Price Index (PPI) – July 2025

Released two days later. PPI final demand rose 0.9% m/m vs 0.2% forecast, lifting y/y to 3.3%, highest since Feb 2025. Services prices up 1.1% m/m, strongest since March 2022. Analysts linked the jump to tariffs. Treasury data showed $113B tariff revenues over three months, nearly 6x last year.

The gap between mild CPI and hot PPI means tariffs are squeezing supply chains. Either costs pass to consumers, raising CPI and forcing Fed hawkishness, or firms cut costs through layoffs and investment cuts. Powell’s remarks implied the Fed expects the latter.

Geopolitics Snapshot

Iran–Israel

After June’s 12-day conflict (Operation Rising Lion) hit Iran’s nuclear and defense assets, tensions remain high. On August 18, Iran’s adviser Safavi warned war could resume at any moment. Internal Iranian messaging is split. Iran is protecting nuclear scientists and bolstering regional proxies, especially Houthis. Arab states condemned Israel’s strikes, freezing normalization talks. Risk of a wider war that could threaten oil flows through Hormuz remains high.

Russia–Ukraine

Russian forces advanced another 25 square miles in Donetsk mid-August, aiming for Kramatorsk. U.S. and Europe press Moscow to negotiate. Trump voiced support for security guarantees but has been inconsistent on ceasefire terms. The Pentagon restricts Ukraine from using long-range U.S. missiles inside Russia. Energy and grain markets remain exposed. Combined casualties exceed one million, signaling a long attritional war.

Commodities and Digital Assets

Crude Oil (WTI)

October 2025 WTI settled $63.77, up on the week. Support came from stronger U.S. PMI, Powell’s dovish tone, the largest inventory draw since June, and geopolitical risks. Bearish side: EIA forecast large Q4 2025–Q1 2026 builds, projecting $58 oil. Weak German data and tariff-driven trade slowdown cap upside. Technically, WTI broke out of a descending channel, with the 50-SMA turning supportive. Resistance at $64.06 and $65.30.

Bitcoin

Bitcoin rallied on Fed dovishness, up 4% Friday. But ETF flows showed $1.17B out over five days, longest streak since April, signaling institutional caution. Tariffs on Chinese mining rigs now at 57.6% duty hit U.S. miners. CleanSpark faces $185M in liabilities, Iris Energy $100M. Ethereum drew capital inflows on ETF expectations, with one whale rotating $75M from Bitcoin to Ether.

Trade ideas

WTI long: Buy dip $62.80–63.00. Target $65.30. Stop below $61.60.

Bitcoin range: Sell near $116k, buy $109-112k.

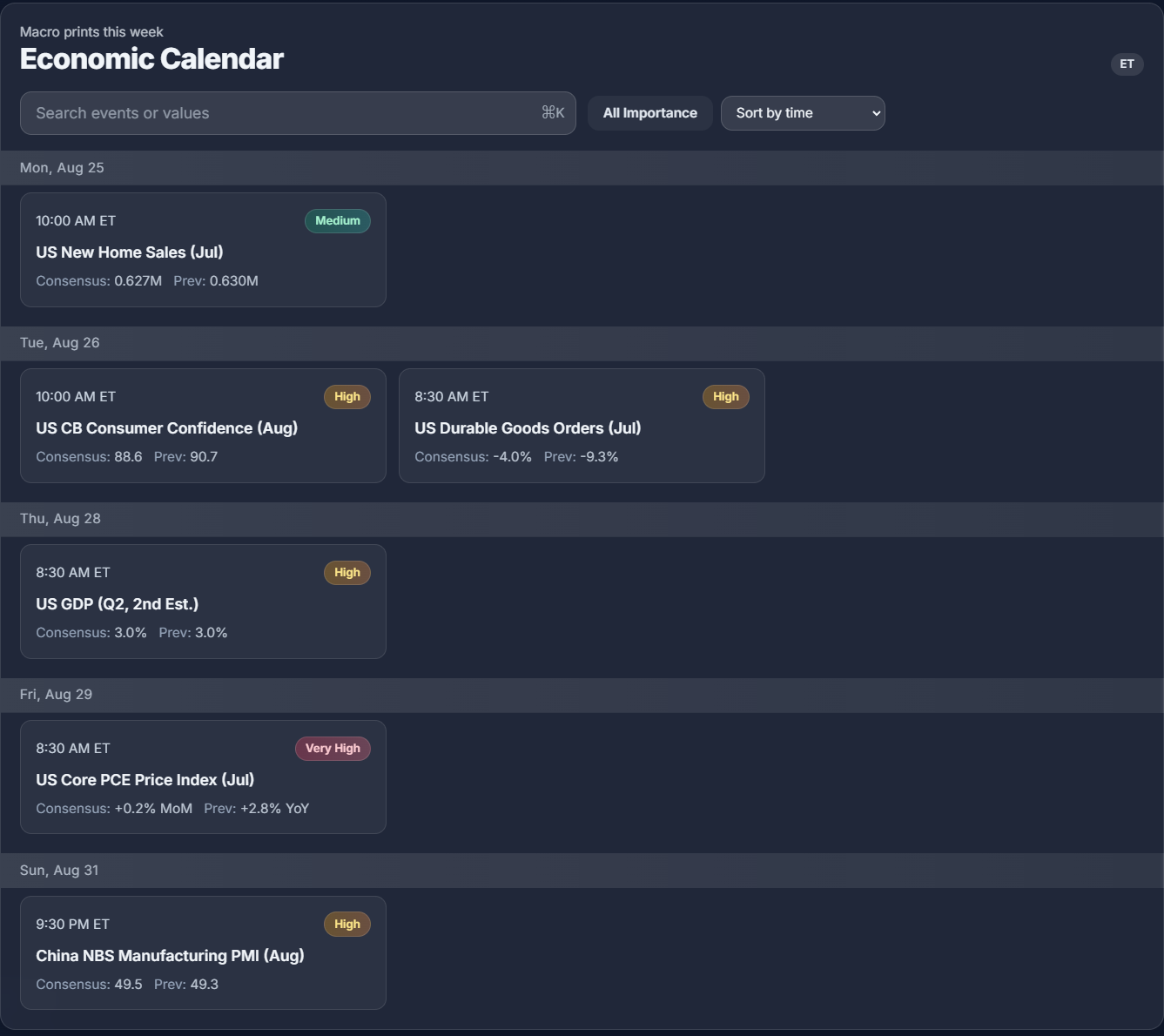

U.S.: July Core PCE (Fed’s preferred gauge) Friday. Hot print challenges September cut; soft print confirms dovish bets. GDP 2nd estimate Thursday. Durable Goods and Consumer Confidence Tuesday.

Global: China NBS PMI Aug 31. Europe August CPI. GDP from Canada and India.

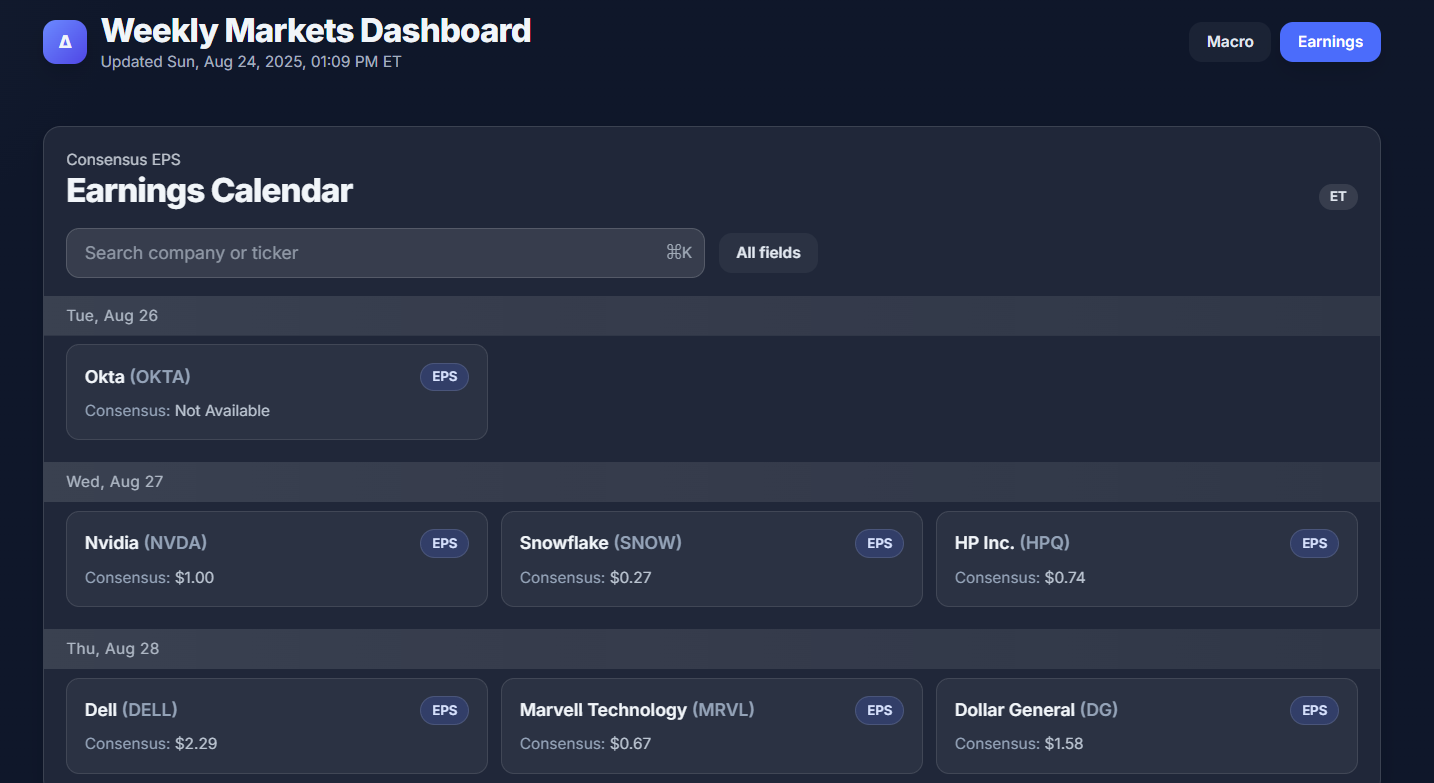

Earnings: Nvidia (Aug 27 after close) expected $1.00 EPS. Guidance on AI chips and U.S.–China trade is macro-critical. Also reporting: Dell, CrowdStrike, Snowflake, Autodesk, Marvell.

WEEKLY LEVELS

Subscribers are urged to use the tradingview indicator to plot the levels.

NOTE: SUBSCRIBERS ARE URGED TO JOIN THE DISCORD AT THEIR EARLIEST CONVENIENCE.

https://sidestack.io/algoflows

Sign in with your Substack email and click the link in your email and you are in.